U.S. Economic and Market Highlights

THE ECONOMY

- The economy looks strong, and in the second quarter, the consensus expects real GDP to grow around 2% in the U.S. Consumption in the first quarter was the strongest since early 2021, powered by the labor market and fading inflation. Food and energy price inflation had hit households particularly hard.

- Multiple forward-looking indicators point to a slowing economy, at best, and are historically leading indicators of a recession. The inverted yield curve reached the one-year mark since it initially inverted. Central Banks remain hawkish, which extends the impact of higher rates on the economy.

- The cost-of-living adjustment (COLA) increase in January was a targeted, short-lived boost to spending. Looking ahead, household consumption could face less financial support. Fed rate hikes are starting to impact the household balance sheet with higher interest payments. Student loan forbearance is coming to an end in the 3rd Quarter.

- Years of interest rates at or close to zero caused government debt issuances to climb significantly. Higher interest rates on current and future debt will have meaningful implications for the government’s ability to provide financial stimulus to help grow the economy in event of a downturn in the business cycle.

FIXED INCOME

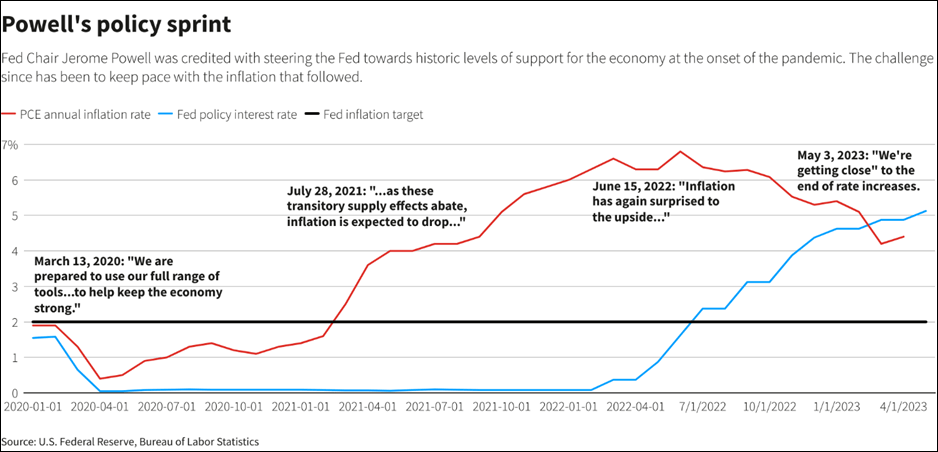

- At mid-year, it may not feel like we are in or approaching a recession. Consumers have been resilient, inflation is slowing and the economy is doing pretty well. But forward-looking indicators are weakening, and the Fed rate hike cycle may not be over.

- Fifteen months and 10 consecutive rate hikes later, the Federal Reserve was content to keep interest rates steady at its June rate-setting meeting. Fed Chair Powell said, “tighter credit likely to weigh on economy.” The threat of recession is making debt securities a safer bet, while the stock market is yet to price in those risks.

- European Central Bank President Christine Lagarde, said “Inflation has been coming down, but it is projected to be too high for too long, the Eurosystem data show that headline inflation will average at 5.4% in 2023, 3% in 2024 and 2.2% in 2025.”

- Higher interest rates resulted in widening yield spreads with lower prices and increased yields on corporate bonds. Investment grade bonds with lower prices and higher yields are popular allocations as investors anticipate an economic slowdown.

- The aggregate bond index was slightly down in June and the yield on the 10-Year U.S. Treasury Note rose above 4% in early July.

EQUITIES

- The S&P 500 is up by more than 20% from its most recent low, marking the start of a bull market, partially triggered by the introduction of artificial intelligence into the mainstream vernacular. However, in former market rebounds (e.g., dot-com and housing crashes), stocks rebounded by over 20% then promptly erased all of those gains.

- Market gains in the 2nd Quarter were heavily skewed toward the largest tech company names. Index concentration is at its highest level since the mid-1970s. Technology stocks are having a bumper year. Despite a recent wobble, the share price of the Big Five—Alphabet, Amazon, Apple, Meta and Microsoft—has jumped by 60% since January, when measured in an equally weighted basket.

- The price-to-earnings ratio (P/E) measures how much the markets think a company is worth relative to its profits. The tech companies are trading at prices multiple-times higher than the median firm in the S&P 500. With P/E ratios above 19x on average in the index, owning stocks (equities) will ultimately have to contend with elevated yields in other asset classes.

- Most returns in worldwide equity markets were negative in May and reversed in June with solid returns in all markets worldwide. All sizes and styles of company stocks did well in June, especially emerging markets in Latin America and Brazil.

- As long as the Fed remains hawkish the U.S. Dollar will retain some strength against other major currencies. The Mexican Peso has appreciated in value because of a steady inflow of remittances, strong export growth, increased capital investment from the United States and China, and a tighter monetary policy with lending interest rates at 11.25% in June 2023.

- Despite China’s reopening after regaining more control over the spread of Covid-19, China’s economy has systemic risks that do not necessarily have simple solutions. China is currently in multiple mild standoffs with its Asian neighbors, overbuilt and undersold real estate, and unpopular government.

- Energy company stock prices are down by 20% YTD while the S&P company index average is up 17% YTD. (See Market Tracker below).

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results. See below reference sources used in preparing the above information.