U.S. Economic and Market Highlights

THE ECONOMY

- The latest U.S. Inflation Report indicates that the Fed’s Approach is working to tame inflation, but slowly. The all-items inflation index increased 5.0% for the 12 months ending March; this was the smallest 12-month increase since May 2021. Core CPI (all-items less food and energy) index rose 5.6% because energy decreased 6.4% and the food prices increased 8.5% over the last year.

- The annual inflation rate in the Euro Area was confirmed at 6.9 percent in March 2023, down for a fifth consecutive month. Inflation in the 20 countries that use the euro currency has slowed to the lowest level in a year.

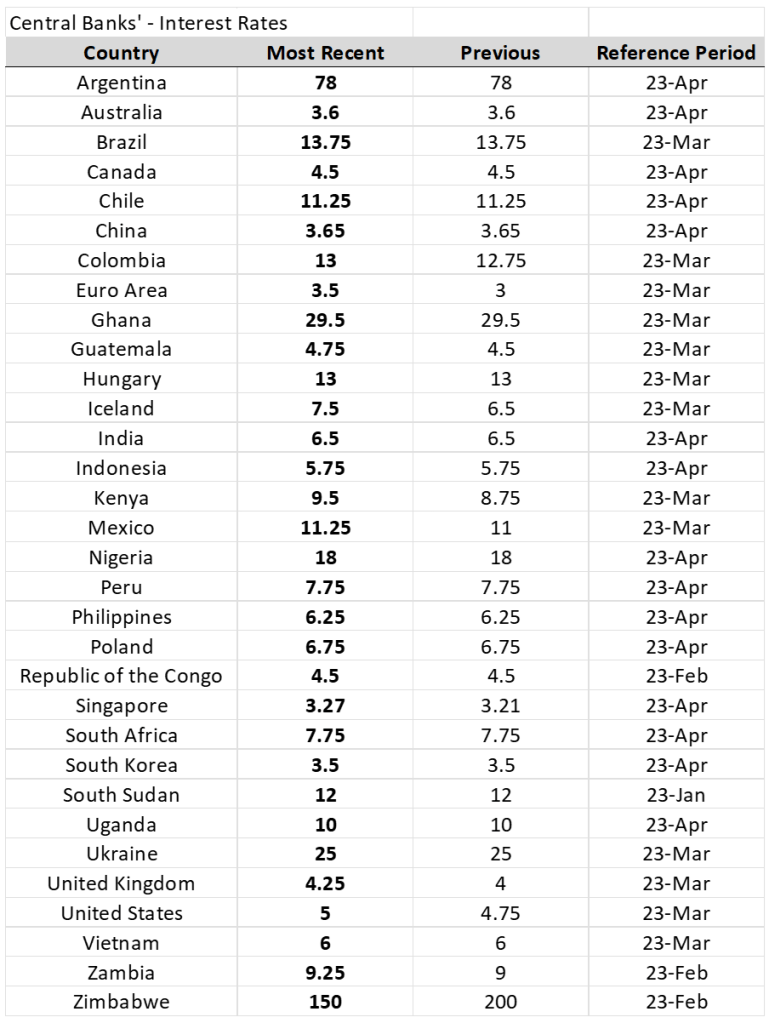

- Central Banks around the globe have indicated that they will focus on the inflation data to determine when to curtail interest rate hikes. Many Central Banks have paused from making additional rate hikes and other Central Banks reduced the size of rate increases at recent meetings. The European Central Bank and Central Bank of Kenya raised the most last month with a 0.50% and 0.75% increase, respectively.

- The International Monetary Fund expects global output growth to fall from 3.4% last year to 2.8% in 2023, before rising to 3% in 2024, mostly unchanged from our January projections. Advanced economies are expected to see an especially pronounced growth slowdown from 2.7% in 2022 to 1.3% in 2023.

FIXED INCOME

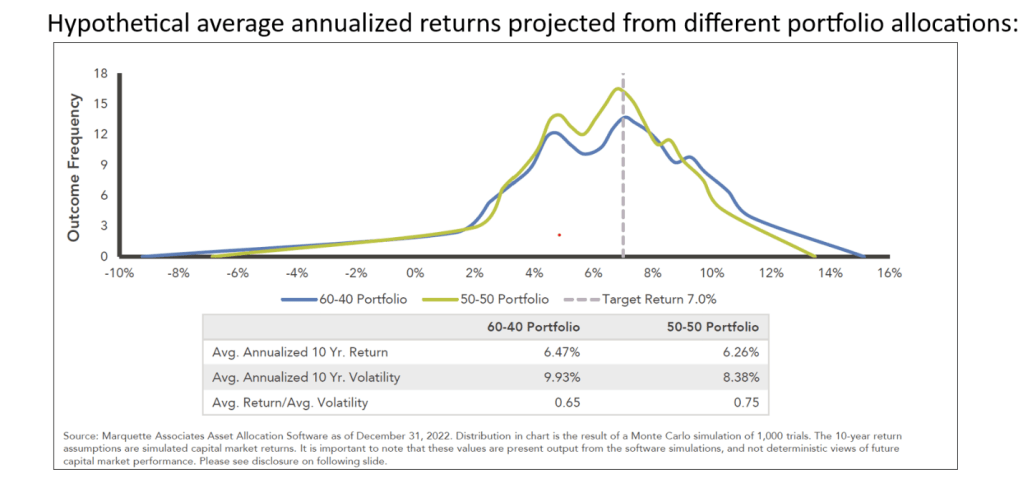

- High quality bonds generally benefit from the traditional qualities of diversification and capital preservation, with the potential for upside price performance in the event of economic deterioration.

- With lower prices and higher yields on fixed income investments, the chart/model below shows that the probability for increasing long-term (risk adjusted) returns improves when allocating more to fixed income in the current market environment (mainly because of lower overall volatility).

Global sales of green bonds (ESG or sustainability-linked bonds) posted the busiest quarter since green bonds first emerged in 2007.

- In Europe, the world’s leading market for ESG bonds, sales of ESG bonds made up 39% of total corporate issuance in the first quarter, up from about 33% during the same period last year.

- However, U.S. sales of ESG bonds are down this year amid pushback on ESG from some state governments. Sales of the ESG bonds as a share of overall issuance have fallen, with ESG debt in the first quarter making up 2.47% of about $248 billion in bonds issued by U.S. companies globally. That compares to about 6.08% sold in the U.S. during the prior-year period.

EQUITIES

- European stocks rallied in the first quarter with double digit returns YTD and a lower average price-to-earning (P/E) ratio than the S&P 500 at 12.6 versus 18.1, respectively, suggesting that European shares look cheap compared to their U.S. counterparts.

- China’s reopening from COVID-19 restrictions has helped European stocks and sectors, especially luxury goods. China’s economy rebounded in the first quarter of 2023, even though there is still weak industrial output, falling property investments, and high stock market volatility.

- Positive corporate earnings released thus far for the first quarter have indicated that companies and their customers/consumers have been resilient in light of higher interest rates and tighter lending practices. The measure of consumer confidence is up from a year ago.

- U.S. stocks also gained in the first quarter, but not without considerable volatility. Growth companies, especially large-cap tech and communication services sectors had the best returns. (See Market Tracker below.)

- Gold rose to approach a record high and cryptocurrencies extended their recovery from 2022’s rout, with Bitcoin and Ethereum both gaining more than 50%.

- The energy sector was the worst performing, down 18.7% YTD (through March). Oil prices were up again in April on OPEC’s announcement to reduce production levels.

- Higher interest rates and the recent banking industry turmoil (bank closures) have led banks toward more cautious and tighter lending practices, which will slow business borrowing and subsequent business/economic growth.

- The primary questions remain – How fast, and how much, will the economic slowdown occur and will it result in a hard or soft landing (recession)?

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results. See below reference sources used in preparing the above information.