U.S. Economic and Market Highlights

THE ECONOMY

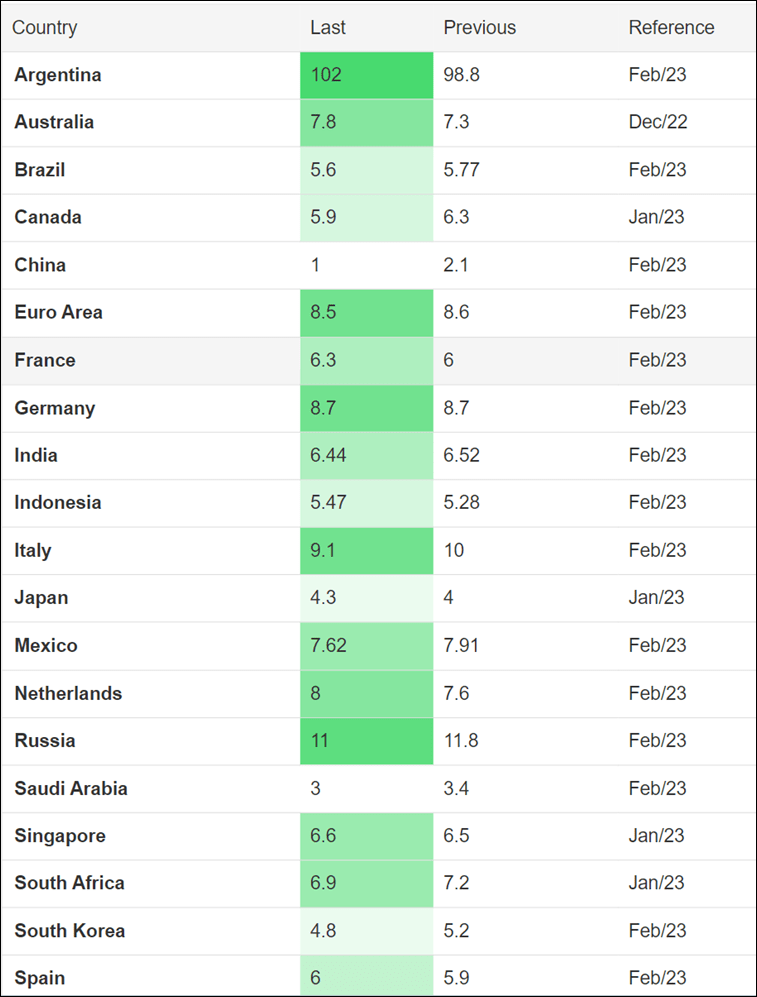

- Annual rate of headline inflation in the U.S. slowed to 6% in February from 6.4% while the annual rate of core inflation moderated to 5.5% from 5.6%. (See below list of inflation data from around the world.)

- While global economic growth as measured by Gross Domestic Product (GDP) is predicted to slow over the next two years, more resilience is expected from developing and emerging market economies whose projected GDP growth is generally above 2022 levels.

- Africa’s average GDP growth is expected to stabilize in 2023-2024, despite recent headwinds. The report, Africa’s Macroeconomic Performance and Outlook 2023, estimates Africa’s average GDP to stabilize at 4% in the next two years, up from 3.8% in 2022.

- The U.S. economy added 311,000 jobs last month, more than expected (300K), while the unemployment rate ticked higher to 3.6%. This news was welcome because a very low unemployment rate can have negative consequences including higher inflation and reduced productivity.

- In Australia the opposite occurred, and the unemployment rate fell to 3.5% a 50-year low as the economy continues to be resilient after nine consecutive interest rate hikes from the Reserve Bank.

- The likelihood of additional rate hikes was elevated based on robust economic data in the first two-months of 2023, until the recent collapse of Silicon Valley Bank (SVB – America’s sixteenth-largest bank) and concerns about the solvency of regional banks at large,became a market moving event for the month of March.

- To avert a potential bank run on other banks that could destabilize the financial system, the Fed and US Treasury Dept. took extensive action to make depositors (at SVB) whole on deposits above the FDIC insurance limit of $250,000. Also, the Swiss National Bank borrowed money to shore up liquidity at Credit Suisse Bank.

- The result of the bank situation may be the turning point for less hawkish rhetoric from Central Banks and a move toward easing or halting further interest rate hikes.

- The Fed has a substantial toolkit to address financial stability concerns, but it would rather use interest-rate decisions to address its employment and inflation objectives.

- The European Central Bank raised short-term interest rates 0.50% (50 bps) this week to continue to slow inflation and support the value of the Euro against other major currencies.

FIXED INCOME

- Historically, protracted inversions of the yield curve have preceded recessions in the U.S. An inverted yield curve reflects investors’ expectations for a decline in longer-term interest rates as a result of deteriorating economic performance.

- In February, fixed income (bond) values and total returns were lower because of rising interest rates and central bankers’ commitment to tame inflation. After two months, the year-to-date return was close to zero for most bond indices.

- Treasury yields fell in March because of waning confidence in the regional banking industry. The yield curve steepened (meaning it was a little less inverted) on the short-end of the curve as the 2-year Treasury yield fell 118bps to 3.89% after reaching 5.07% a week ago, while the 10-year Treasury yield decreased 53bps from 3.99% to 3.46%.

- Prior to the recent bank failures, a significant portion of domestic banks tightened lending standards to lower the risks of loan defaults in a higher interest rate environment. The banking stresses this week indicate that higher interest rates have had a significant impact on the banking infrastructure and will likely reach the intended result of slower business activity in 2023.

- Perhaps the monetary supply and demand balance will be reached, and interest rate hikes will be put on pause in the near future. This week may be a turning point, as central banks and large commercial banks provided additional liquidity stimulus through newly established deposit and funding programs to lessen the impact of higher interest rates on the broader banking industry.

EQUITIES

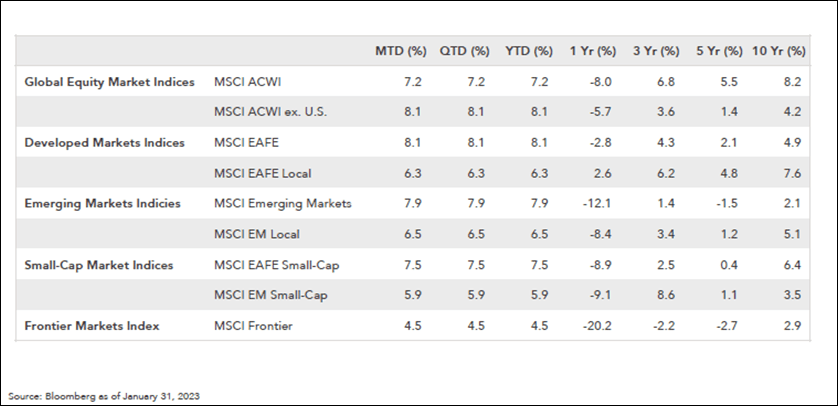

- International equities (stocks) started the year on a strong note. The global indices rebounded in January followed by a decline in February.

Global Markets – January 31, 2023

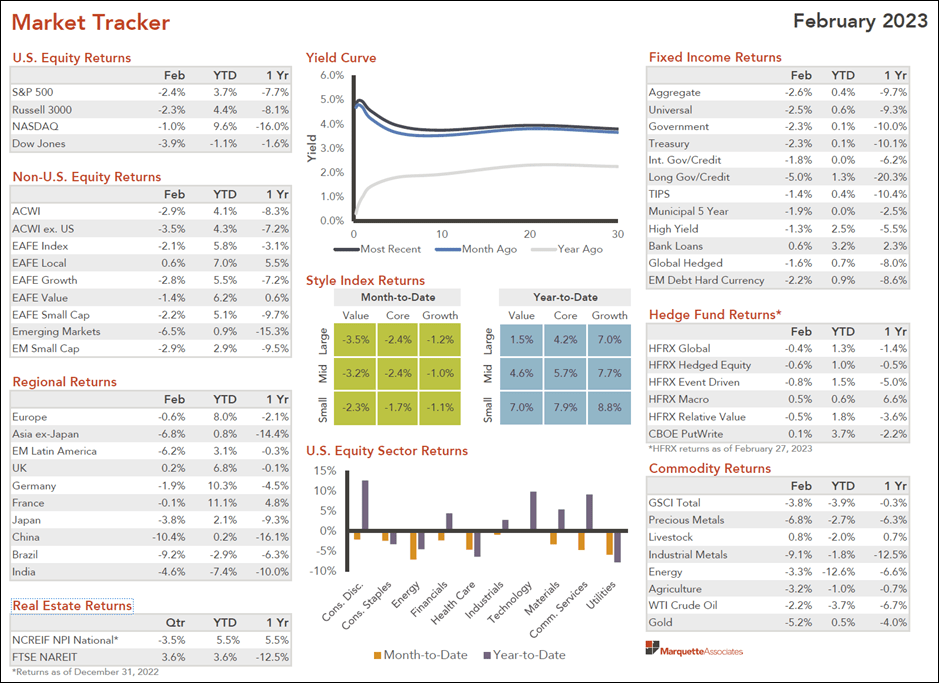

- Stock markets around the world were down in February on fears that persistent inflationary pressures would drive interest rates higher increasing the likelihood of a recession. (See the Market Tracker below.)

- In March, stock prices continue to decline with the banking industry scare coming on the heels of hawkish Fed rhetoric and higher than comfortable inflation rates.

- University of Michigan’s consumer sentiment index fell to 63.4 in March from February’s reading of 67.0. Companies’ earnings’ expectations are lower after ending the year on the decline.

- Total returns were in property sectors and REITs were down by double- digits in 2022 with growing dividend rates. Liquidity is limited for shareholder redemptions in real estate funds as values are down with higher interest rates and cost of capital.

Source: Trading Economics

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results. See below reference sources used in preparing the above information.