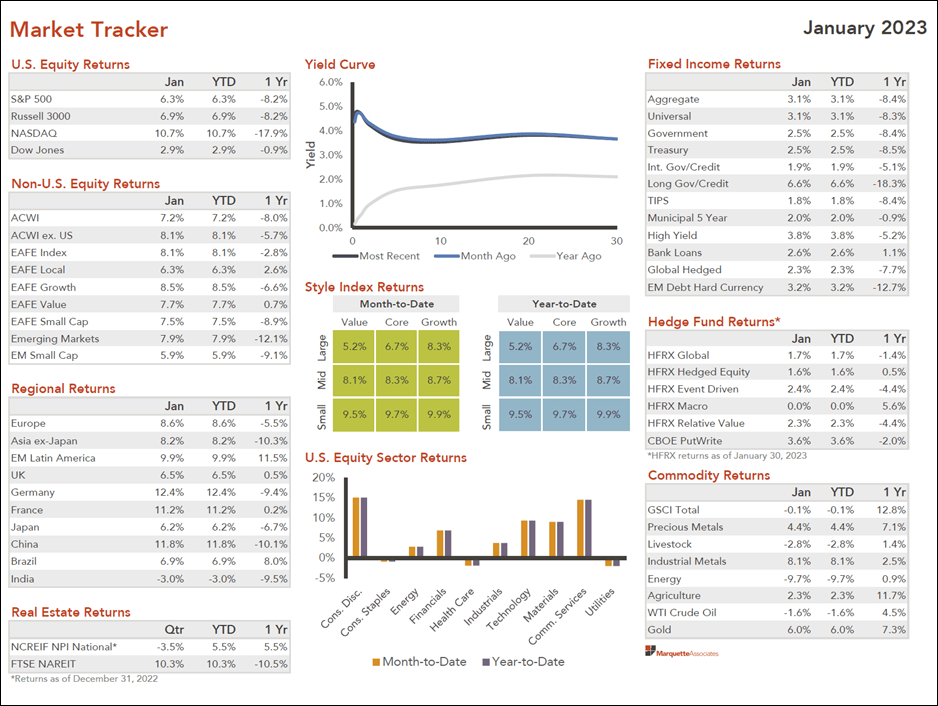

U.S. Economic and Market Highlights

THE ECONOMY

- The U.S. labor market surprised investors with a strong month in January, adding 517,000 jobs which reduced the unemployment rate to 3.4%.

- As economic trends have started to revert back to longer-term averages, the strong jobs report put into question how long inflationary conditions will persist and how high will the Federal Reserve need to raise short-term interest rates.

- The January year-on-year headline and core inflation rates slowed to 6.4% (from 6.5%) and 5.6% (from 5.7%) respectively, slightly higher than expected in part because of rising gas and fuel prices.

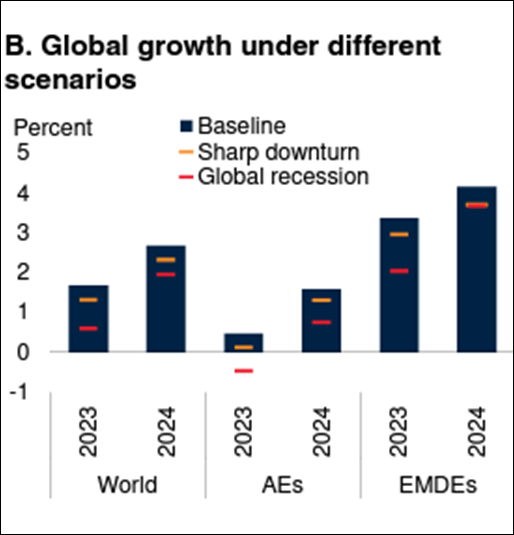

- The World Banks’ Global Economics Prospect report shows data under different scenarios, with the baseline being favorable to a mild recession this year with recovery trajectories including economic growth, lower inflation rates, and stable supply chains.

- Gross Domestic Product (GDP) projections above show a baseline estimate based on recent data and trends, and mostly positive GDP figures in 2022. Samples of GDP growth rates from various countries for 2022:

– US GDP rose 2.9%.

– Italy GDP rose 3.9% (preliminary).

– Poland GDP rose 3.3% (three-year average).

– Mexico GDP rose 3.0%

– India GDP rose 7.0% (est.)

– Indonesia GDP rose 5.3% (best since 2013).

– Philippines GDP rose 7.2%.

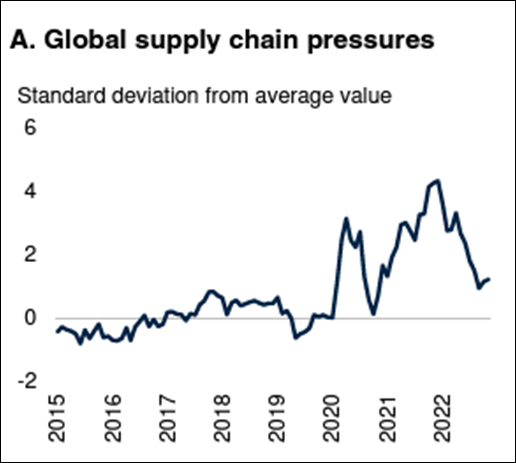

- The economic transition will continue in 2023, likely including recovery from COVID-19, supply chain disruptions, outbreak of war in Eastern Europe, global inflationary pressures, and higher interest rates.

- The baseline estimate is that some economies will experience recessionary conditions, especially in advanced economies who are projecting the lowest growth rates. Emerging markets and developing economies are expected to have higher growth rates in 2023.

FIXED INCOME

- February’s price action so far has been mostly a reaction to strong nonfarm payrolls data in the U.S.. Longer-term Treasury yields increased with the stronger economic data and hawkish commentary by the Fed and European Central Bank (ECB) officials.

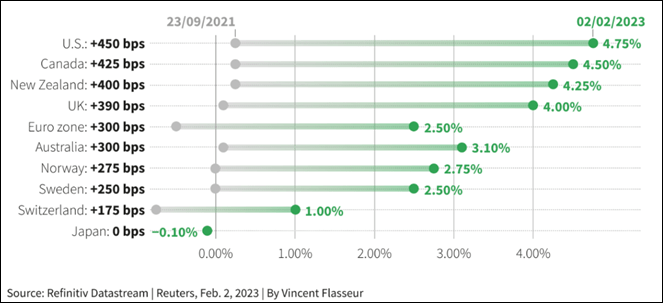

- Also in February, the Fed increased short-term rates by 0.25% and the ECB increased rates by 0.50%. The ECB lags the Fed in the level of rate hikes since almost a year ago when the outbreak of war exacerbated the inflation rates and forced central bankers to react.

- The US Dollar strength remains somewhat intact after a slight decline in relative strength against other major currencies over the last several months. Currency exchange rate fluctuations correlate with the likelihood that central banks will increase short-term interest rates again near-term.

Rate hikes from a sampling of Central Banks since March 2022 to Feb. 2, 2023

- Global bond market rebounds strongly in January as inflation fears receded last month. The Bloomberg Aggregate Bond index was up 3.1% in January (see the Market Tracker below). Fixed income is recovering from last year’s record-breaking rout, restoring its traditional role as a haven against economic downturn with some yield in return.

- Bond investors are somewhat buffered against the impact of recessionary conditions because central banks are expected to slow that pace of rate tightening near-term and cut rates in 2023, as economies continue to slow. As yields decline, existing bond prices generally increase compared to new issuances at lower rates.

- If companies credit ratings and consumer confidence are not hurt too badly from the anticipated economic slowdown, then bond values and yields should not be disrupted significantly.

EQUITIES

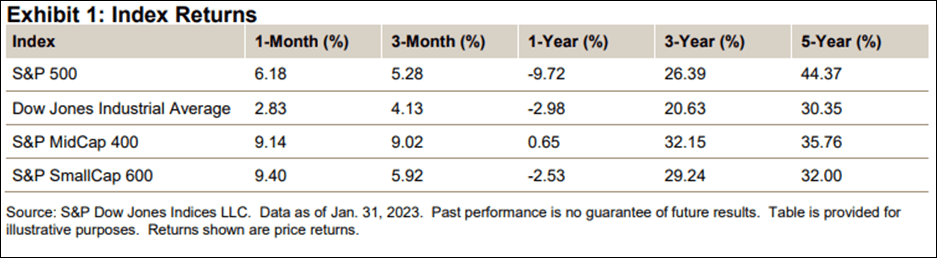

- It was the first January gain for stock markets in four years after three years of January declines. While the start of the year was positive, the stock market indices still have a way to go to make up for last year’s decline.

- A happy January tends to make for a happy year, as the saying “so goes January, so goes the year” has historically been correct 71% of the time.

All capitalization categories were up for the month of January as small-caps outperformed large-cap stocks and growth stocks slightly outperformed value.

- All sectors globally produced positive returns to start the year. Information

Technology stocks exhibited a strong comeback.

- Growing trade and geo-political tensions between the U.S. and China and the U.S. and Russia has led to more regional economic integration which involves more investments between the U.S., Mexico, and other Latin American countries.

- Mexico’s stock market had the strongest performance of the MSCI ACWI ex-U.S. Index returns with a January return above 15%.

- Commodities were mixed with precious metals, industrial metals, and gold rising during the month of January in anticipation of a reversal in the trajectory of interest rates. Gold is highly sensitive to rising U.S. interest rates, as rates increase the opportunity cost of holding non-yielding bullion rises.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results. See below reference sources used in preparing the above information.