U.S. Economic and Market Highlights

THE ECONOMY

- U.S. consumer price increases, measured by the CPI, ended the year up 6.5% year-on-year in December, moderating from a 7.1% rise in November. This was welcome news as inflation rates continue to decline.

- The real economy has yet to fully adjust, with a modest recession likely in 2023 and uncertainty about how much unemployment will rise. U.S. unemployment rates dropped in December to 3.5% and wage rates increased to 6% per annum in December, further exacerbating the need for the Fed to stay vigilant on monetary tightening.

- See the memorandum attached about recessions and their historical impact on the stock and bond markets.

- Eurozone headline inflation is on the decline faster than previously expected and forecasts from major investment banks are that GDP in Europe will be positive in 2023, in part because of lower energy prices and the reopening of China’s economy (from Covid lockdowns) underscoring the likelihood of a better-than-expected year for Europe’s major industrial exporters.

- China’s economy was more resilient than expected as GDP grew 3% in 2022 and shows signs of upward growth in 2023. India’s population trend is expected to result in accelerated economic growth in the coming decade at an average pace of 6.5% per year.

- The above economic trends led to a significantly weaker U.S. Dollar in comparison to other major currencies over the past month.

FIXED INCOME

- Central banks are slowing the pace of rate hikes as inflation rates subside, with the Fed expected to raise again by 25-basis-points in February, following seven consecutive rate hikes in 2022 bringing the policy rate to near 4.50%.

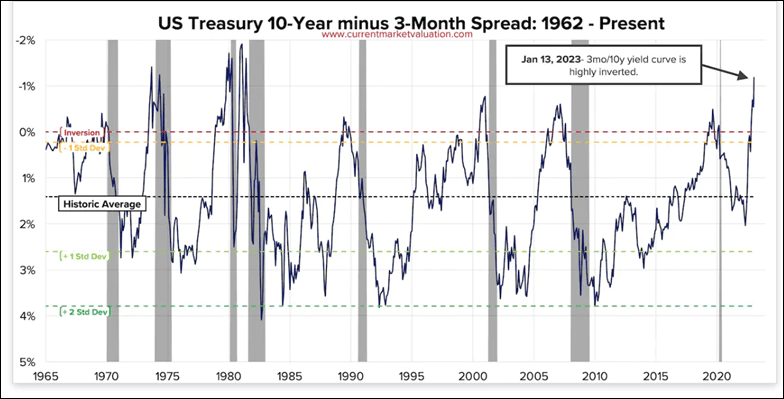

- With short-term interest rates exceeding long-term rates by a significant margin the inverted yield curve points toward a recession in 2023.

- With rising interest rates, 2022 was a rough year for bonds. But, with rates near the peak, fixed income investors are seeing opportunities to add duration to their portfolios, in anticipation of lower rates in the coming quarters.

- A white paper issued by T. Rowe Price argues that fixed income markets offer opportunities that can potentially help support investors with a range of goals and risk tolerances. Bonds look much more attractive now than they have in a long time with higher yields and the potential to provide resilience and diversification across a range of economic outcomes.

- The price declines in 2022 provide an opportunity for investors to now buy similar bonds at significant discounts to last year’s prices. Also, investors can find blue-chip, quality bonds globally, yielding over 5% without needing to take on a lot of risk.

- Other attractive subsectors within fixed income are agency mortgage-backed securities, securitized products, and other high-quality fixed income assets. That is why flows into Europe high-grade bond funds ended the year with 10 consecutive weeks of inflows, a trend that’s expected to spread to the U.S..

EQUITIES

- Hopes that the Fed could soon ease back on its aggressive tightening after raising the federal funds rate seven times in 2022 have boosted the market in recent sessions, even as comments by some Fed officials have supported the view that the central bank will remain vigilant about raising rates to fight inflation.

- Small-cap stocks outperform so far in 2023 as the Russell 2000 (Small-cap) index was up 7.1% versus the S&P 500 (large-cap) index, which rose 4.2% in the first two weeks of the year. Small-cap stocks typically tend to lead in the second half of interest-rate tightening cycles.

- Also, the general cyclical positioning and macroeconomic fundamentals of Emerging Markets (EM) seem to favor EM companies compared to companies in developed markets. (See Market Tracker below.)

- EM markets vary widely but are generally further ahead of developed markets in their monetary tightening and equity derating cycles. Brazil, Mexico, and other Latin American countries began raising interest rates well before the United States and Europe. All these countries exhibit positive real interest rates (bond yields minus inflation), unlike the United States and Europe.

- Given the combination of price declines, the derating of valuation multiples, and earnings estimate cuts, EM equity markets may have already readjusted and are better positioned for recovery than developed markets where the negative earnings revisions process has just recently begun, especially with expectations for interest-rate cuts and other stimulative measures to come in 2023.

- As an asset class, the relative performance of emerging markets tends to be negatively correlated with a strong U.S. dollar. If the U.S. Dollar is close to peaking, that would be another bullish signal for EM equities. The most promising EM equity markets in early 2023 are China, India, Brazil, and Indonesia.

- As rising interest rates favored value stocks, declining rates tend to favor growth stocks because companies with positive momentum are more likely to continue to grow as the economy slows, in comparison to cyclical companies, and benefit from the rebound that occurs from lower interest rates in the later stages of a recession.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results. See below reference sources used in preparing the above information.