U.S. Economic and Market Highlights

THE ECONOMY

- The U.S. Core CPI inflation rate dropped to 6.0% year-on-year, and headline inflation (including energy and food) dropped to 7.1% in November favorably below expectations.

- The Federal Reserve pushed back against the softening inflation trend with a hawkish 0.50% (50 bps.) rate hike saying that they want more evidence that inflation is slowing before they stop raising interest rates to tighten financial conditions.

- Continued hawkishness is likely to stem from the recent decline in Treasury yields and the declining USD exchange rate which do not support the Fed’s fight against inflation.

- The Fed is likely not finished raising interest rates, but if the declining inflation rate trend continues, future rate hikes will be more of a hedge or insurance increase rather than sounding the panic alarm.

- The European Central Bank also raised rates 0.50% and committed to keeping interest rates at a restrictive level to reduce inflation to its 2% target.

- The tight labor market in the U.S. and relatively optimistic growth outlook globally, increases the likelihood of further rate hikes from Central Banks, which will dampen the outlook of capital markets because of the increased possibility for recessionary conditions to follow six months hence.

- In 2022, the 2-year Treasury yield increased from 0.78 to 4.23% and the 10-year Treasury yield increased from 1.63 to 3.49% year-to-date, thus resulting in a current inverted yield curve with a 0.74% inverted spread.

- The effects of the increased rates and inverted yield curve will dampen housing, consumer spending, and other sectors. November’s retail sales figures dropped well below expectations and corporate layoffs have picked-up in recent weeks.

- Equity investors are hoping that inflation continues to decline, and that Central Bankers’ rhetoric is more aggressive than their near-term monetary policy actions.

FIXED INCOME

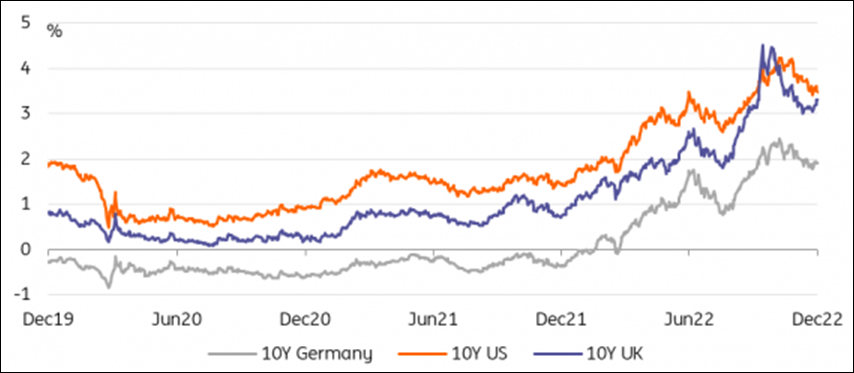

- The 10-year Treasury Bond and 10-year German Bund yields dropped more than 15% each over the last five weeks as inflation rates decline. Declining long-term yields last month resulted in a fixed income market rally in November. (See line chart below.)

- The outlook for bonds looks better for 2023, after it experiences the worst 12-month period ever. That is not to say that yields on the long-term bonds won’t continue to be volatile as many uncertainties regarding inflation, monetary policies, and geo-political risks persist.

- Mortgage rates rose sharply in 2022, above the record low rates in 2020 and 2021, reaching close to 7% in the U.S. in October on 30-year mortgages. This is the highest level in decades, but still slightly below the average of 7.8% over the last 50 years.

- Home prices are down amid soaring mortgage rates and a pullback in transactions and private sector rent indices are also retreating.

- Real Estate Funds have experienced record high redemptions in the fourth quarter as investors pull profits off the table in one of the only positive asset classes this year.

- Higher interest rates delivered higher coupon rates on newly issued bonds. This outcome has created a path for longer-term tailwinds for Investment-Grade (IG) credit going forward.

- Even if there is a recession, the probability of default for IG issuers is low.

- Higher-quality fixed income sectors, like IG, will likely get the benefit of higher yields and duration as a potential defensive mitigator to possible spread volatility if economies enter a recession.

- In a recession, Government bond yields will likely rally, which can provide a big positive boost to total returns.

EQUITY

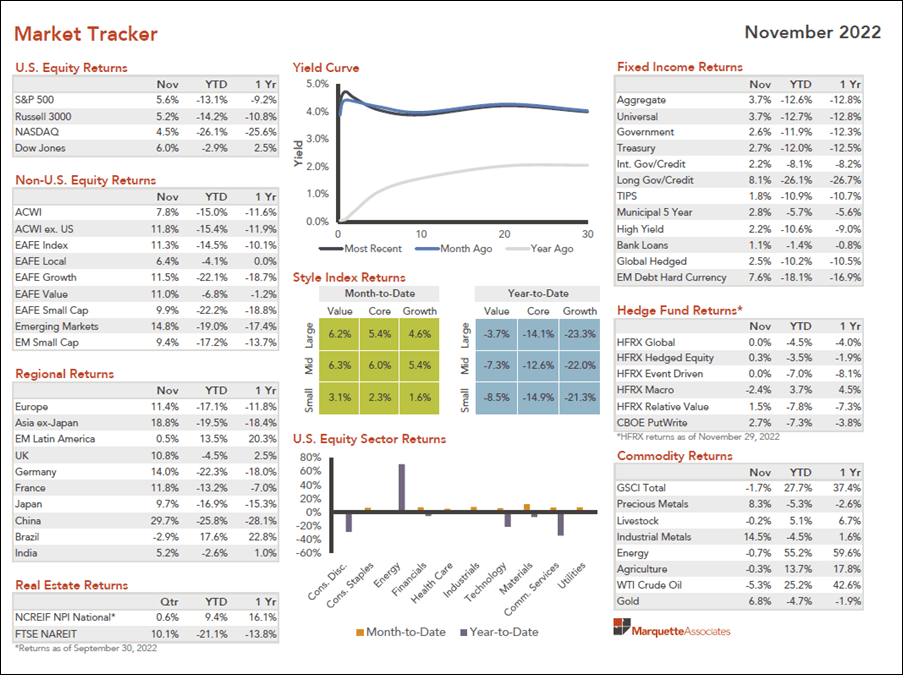

- Equity markets were up in October and November on indications that inflation is abating, and that Central Banks may slow or stop interest rate hikes. (See Market Tracker below.)

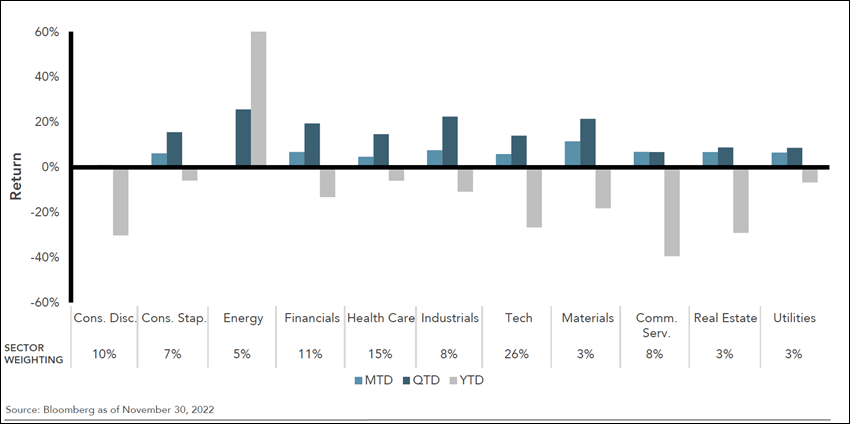

- All sectors were positive in November and so far in the fourth quarter, after negative year-to-date returns in all sectors except energy. (See bar chart below.)

- Corporate earnings estimates have come down in most sectors since the beginning of the fourth quarter.

- Higher yielding (i.e., dividend-paying shares), lower volatility, and value-oriented companies outperformed growth companies which continue to struggle with negative returns.

- Non-U.S. currency performance rebounded in November, led by developed markets that were up 4.6% for the month. Emerging market currencies were up 3.6%.

- Equity markets sold off in early December as the likelihood of a recession in 2023 increases due somewhat sticky inflation data, hawkish Central Banks, and slowing economic and business news around the world. This combination of factors lessens the likelihood of a ‘soft/softish’ landing (or very mild recession).

- During a recession, businesses usually experience decreased demand for their products or services. As a result, they may cut back on production, which leads to layoffs and reduced consumer spending. Equity shares are more prone to negative performance returns and increased volatility. The exception would be companies who are able to proactively adapt or react to the economic slow-down and take advantage of opportunities left by others.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results. See below reference sources used in preparing the above information.