U.S. Economic and Market Highlights

THE ECONOMY

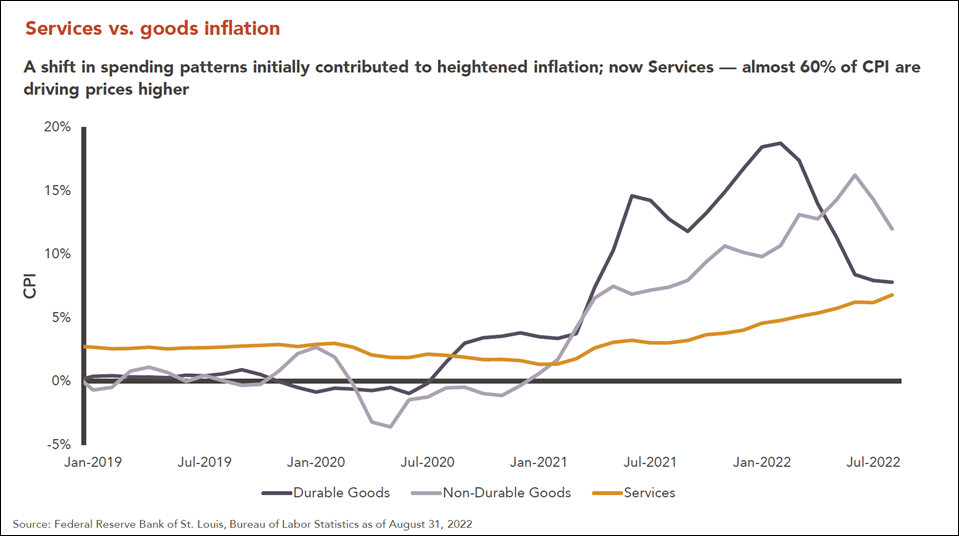

- October’s inflation rate in the U.S. was the lowest year-over-year increase since January at 7.7% indicating a downward trend. Core inflation (CPI excluding food and energy) came in at 6.3% y-o-y also below expectations.

- The Fed delivered its fourth straight 75bps hike and repeated that it anticipates “ongoing increases” but added a qualifier that it will aim for tightening that is “sufficiently restrictive” to return inflation to 2% over time.

- Strong U.S. employment data supported the Fed’s policy stance, as job openings in September rose month-over-month more than expected. Wages and benefits, measured by the employment cost index, increased in the third quarter by 5% year-over-year.

- Some Central Banks (e.g. Poland, Australia, Czech Republic) have slowed, or put on hold, interest rate hikes in hopes of orchestrating a “soft landing” while running the risk of extending the time frame needed to fight inflation.

- The labor market is a lagging indicator and is likely to shift downward as more and more companies are expected to make announcements of layoffs starting with technology companies. This is likely to lead to recessionary conditions in 2023.

- Energy prices have declined, but companies are still trying to pass along higher energy prices where possible including airfares, utilities, and public transportation costs which will keep the core inflation rate higher for longer.

- When rising interest rates have filtered through the broader economy it will negatively impact growth rates of economic sectors, such as real estate.

- Mortgage rates have risen so much that refi and mortgage lending businesses have come to a halt. Increase costs on floating rate mortgages and higher rents will squeeze consumers and ultimately slow down the economy and lead to a reversal of the Central Bankers’ monetary policies, hopefully before too much damage is done.

- Capital markets fear that the Fed will raise interest rates too much and over-shoot their targets, which will result in a rapid decline in economic growth or a “hard landing” which will lead to excessive lay-offs, closures, and negative economic growth.

- Gross Domestic Product (GDP) increased at an annual rate of 2.6 percent in the third quarter and is expected to end the year at 1.5% year-over-year for 2022. Consumer sentiment in the U.S. was revised slightly higher in October of 2022 from the previous estimate.

FIXED INCOME

- Bond market yields have continued to rise as the Ten-Year Treasury Bond yield rose to 4.14% in early November and the Two-Year Treasury Bond yield rose to 4.78% further expanding the inverse yield curve, which is also an indication of a recession.

- When rising interest rates have filtered through the broader economy it will negatively impact growth rates, interest rates will fall, and prices will increase on recently issued, higher yielding bonds. Rates of return on bonds are expected to be very favorable under this scenario from both an interest rate and price appreciation standpoint. It is something that bond investors are looking forward to.

- Corporate credit fundamentals remain strong even though credit metrics are beginning to show a slowdown in activity due to higher interest rates. Investment grade and high yield companies are still in a good position to service their debt.

- After a long period of low interest rates and tight spreads (between the yield on corporate bonds and risk-free Treasury rates), recent bond market underperformance has created a more attractive entry point. Spreads in many sectors now trade at long-term averages or wider.

- Yields on high yield bonds have risen almost double in the last couple of years. For example, a recent Ford Motor credit priced a 5-year bond at 7.85% compared to a similar bond in 2020 at a yield closer to 4%. The Bloomberg High Yield Index has a current yield of 8.99%.

- Returns from commercial real estate investment have started to moderate because of higher interest rates and the prospects for slower economic growth. Strong tenet demand in the multi-family housing will provide financial stability.

- Infrastructure investments have a particular focus on clean energy and energy transition. Accelerating energy innovation supported by the Inflation Reduction Act will help finance these investments. Infrastructure has produced higher yields than traditional markets in recent years.

EQUITY

- Equity markets rebounded in October with the S&P 500 Index up over 8% and the global market (excluding the U.S.) was up 3%. Europe’s equity market was up 7.3% and Latin America was up 9.7% in October. China was noticeably different with a negative return of almost 17%. (See Market Tracker chart below.)

- Value style companies led by the energy sector outperformed growth companies such as technology and consumer discretionary in October continuing the trend for the year.

- With declining stock prices in 2022, Price/Earnings (P/E) ratios have normalized relative to historical ranges; small-cap stocks look particularly attractive. Companies generally show better earnings in in the fourth quarter and following elections.

- Rising rates and the potential for a global economic slow-down has led to a significant increase in the relative value of the U.S. Dollar compared to other major currencies. The stronger dollar increases costs for non-U.S. companies including interest payments, goods, and services. Investors from the U.S. are negatively impacted because the returns they receive from non-U.S. companies convert into few dollars.

- Valuations of non-U.S. equities are at historical lows based on most measures. Non-U.S. developed markets are especially cheap because of equity price declines in 2022. These levels provide support for optimism toward strong medium-to-long-term returns.

- The VIX (Stock Volatility Index) exhibited elevated levels during the last several months amid continued market turbulence, generally remaining above its 20-year average.

- Hedge funds have provided protection against equity market volatility in 2022 capturing just 20% of the market’s downside on a monthly basis with the returns in the various hedge fund indices only down in the single-digits year-to-date, much better than the broader market of equities.

- Private equity and private credit investments have outperformed public markets in 2022. Pooled funds of private companies provide alternative strategies to the public equity and fixed income markets. The lower return correlation to public markets and long-term investment time horizons has served to reduce volatility in institutional portfolios.

- Geopolitical political risks remain high as Russia’s invasion of Ukraine remains a significant headwind. A breakdown of economic relations with China is a possible headwind and COVID and government policies remain risks to global growth.

- Russia announced a withdrawal of its troops from the southern Ukrainian regional capital of Kherson and surrounding areas, a major victory for Ukraine in its efforts to oust Russian troops from its territory.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.