U.S. Economic and Market Highlights

THE ECONOMY

- This week’s inflation reports are likely to show some declines in the headline CPI rate, but concerns will persist if the core CPI rate increases (not including energy and food).

- The Fed set core CPI at +0.5% for both September and October. If core inflation is at 0.5% month-on-month, if sustained, that translates to over 6% year-on-year inflation.

- Recent strong jobs’ report and declining unemployment in the U.S. has provided leeway for the Fed to continue to aggressively raise rates to combat inflation. Another 0.75% hike is likely at the November Fed meeting.

- The Organization for Economic Cooperation and Development (OECD) lowered its projection of the GDP (Gross Domestic Product) growth rate in the U.S. by a full percentage-point to 1.5% for 2022. The estimated growth rate for 2023 was lowered to 0.5%.

- The OECD maintained the global GDP growth rate at 3 percent for 2022, but slashed the 2023 rate by 0.6 percent, to 2.2 percent.

- GDP was negative in the first half of the year in the U.S. and GDI (Gross Domestic Income) has remained positive. Conflicting data makes it more difficult to determine the impact of rising interest rates.

- The ECB (European Central Bank) is raising interest rates while at the same time considering other measures such as Quantitative Tightening (QT) to reduce the size of their balance sheet and combat inflation. Bond yields have increased significantly in recent months without any QT.

- More pressure is being put on European governments to deliver additional fiscal stimulus support to offset the slowing economy and high fuel prices due to the Russian invasion of Ukraine. QT at the current juncture could trigger an unwarranted widening of bond spreads, lower asset values, and a new euro crisis.

FIXED INCOME

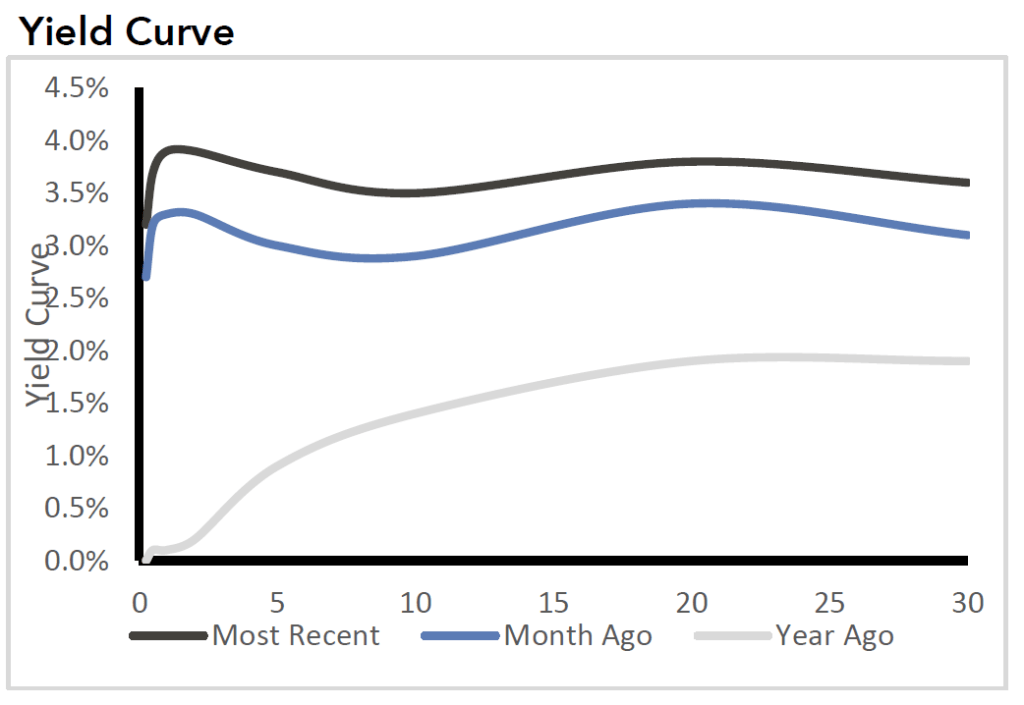

- As interest rates rise, fixed income yields become more attractive, for the first time in quite a while. Income investors are likely to be considering opportunities to invest given the higher yields and lower prices, depending on their outlook and expectations.

- Yields in the U.S. have increased across the entire yield curve.

- Higher yields have come at a cost. Rising interest rates have depressed current values on fixed income portfolios, as previously purchased bonds with lower coupon rates are trading at discounted values. Year-to-date negative returns on fixed income investments are at record levels. (See Market Tracker below.)

- Even though credit spreads for both U.S and European corporate bonds have widened considerably this year (resulting in lower corporate bond prices), fundamental credit quality is proving resilient to this point, with favorable ratings and low default levels due to favorable borrowing conditions preceding 2022.

- Recent market volatility has occurred in response to new or developing fundamental stressors relating to protracted inflationary pressure, higher interest rates, and lower growth and earnings forecasts.

- Acute market stress from price volatility generally appears during or before a recession, which ultimately can result in ratings downgrades and increased defaults. Lower-rated issuers would likely be the most vulnerable if there are liquidity constraints due to recessionary conditions.

EQUITY

- Equity prices experienced a significant decline in September pushing YTD returns into bear market territory of negative 20% or more. The reasons for the decline are the same as those mentioned above – protracted inflation, higher interest rates, and lower growth and earnings forecasts.

- The U.S. ISM Manufacturing PMI index is at a current level of 50.90, down from 52.80 last month and down from 61.10 one year ago. This decline indicates weaker demand for manufactured products. PMI below 50 signifies a shrinking of the manufacturing economy.

- Half of the CEOs (51%) in the U.S. say they’re considering workforce reductions during the next six months. In the global survey overall, eight in ten CEOs say the same. Nine in ten CEOs in the U.S. (91%) believe a recession will arrive in the coming 12 months. The expected severity of the downturn remains uncertain.

- The correlation between stock market performance and midterm elections is well documented. In 17 of the 19 midterms since 1946, the market performed better in the six months following an election than it did in the six months leading up to it. Stocks tend to outperform after midterm elections. Will the trend hold after the election on November 8, 2022? This year’s market performance has already diverged significantly from the average midterm election year.

- The U.S. Dollar continued to strengthen primarily because of the rapid interest rate increases by the Federal Reserve. The strong USD hurts U.S. exporters as cost of goods rise and sales to non-USD importers decline. The relative strength of the USD has disproportionately impacted developed markets more than emerging market currencies.

- China’s real estate sector has lost 63% since December 2019; while the sector makes up only 4% of the MSCI China Index, it represents roughly 30% of the country’s GDP. GDP forecasts have been reduced accordingly. The decline represents the slowest period for the real estate sector since the Global Financial Crisis in 2008.

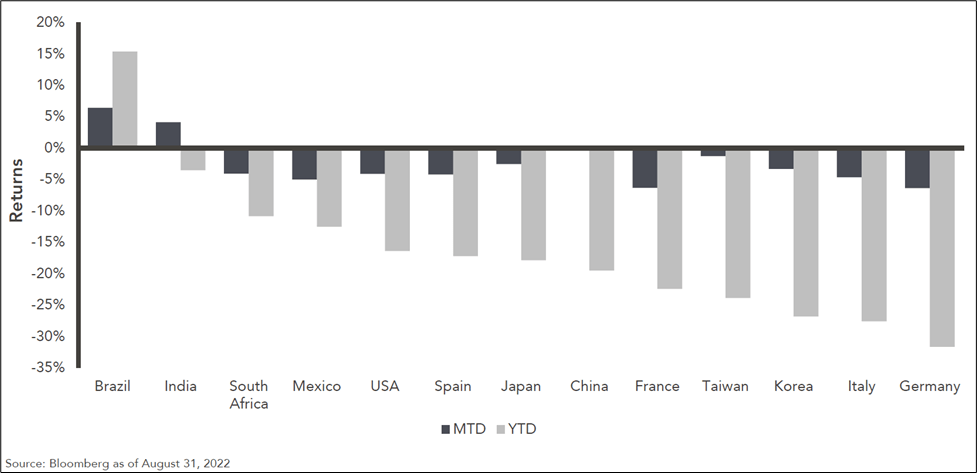

- Brazilian equities have benefited from strong commodity prices and a resilient economy. See chart below.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.