U.S. Economic and Market Highlights

THE ECONOMY

- It has been a roller coaster ride for the last several years. The Real GDP (Gross Domestic Product) growth rates demonstrate this on the following line chart for the World (Data from The World Bank – June 2022).

- Negative GDP in 2020 was due to the global Covid-19 outbreak. Excessive growth in 2021 was due to the government stimulus and pandemic recovery. The 2022 GDP forecast was just revised downward because of the slow-growth outlook caused by Central Bank interest rate hikes in response to inflation and crisis caused by the Russian invasion in Ukraine.

- There is little good news to report short-term, except that the cycle of change continues, and the expected global GDP growth rate forecasted for 2023 is back to 2.8%, the closest it has been to a normal rate in almost five years (albeit a little lower than 2017 and 2018).

- Central Banks around the world have intensified their rate tightening efforts as previously promised as a result of persistently high inflation in recent quarters. The impact of raising rates (besides its intended purpose to slow inflation trends) is slower economic growth.

- As the actions of Central Banks’ short-term rate increases take hold, bond yields on the long-end (e.g., U.S. 10-Year Treasury Note) have dropped significantly in recent weeks from 3.48% in mid-June to 2.80% this week. The rising short-term rate (2-Year Treasury Note at 3.10%) and decreasing long-term rate scenario have increased the prospects for a recession (indicated by an inverted yield curve when short rates are higher than long-term rates).

- This turnaround of events of lower long-term bond yields coupled with signs of lower commodity prices (including gold and crude oil) and the stronger U.S. Dollar has prompted the FED to predict a time when they will be cutting rates again, in the not-too-distant future.

- This change of narrative has a risk of confusing investors. However, optimists believe that the Fed’s approach could achieve an economic “soft-landing” and avoid a significant economic slowdown while taming inflation.

- The Eurozone has additional challenges with a reliance on high-priced fuel from Russia, impact from supply chain disruptions, mass migration of war refugees, and devaluation of the Euro currency.

- The ECB (Central Bank) is expected to start raising short-term interest rates this summer and has already tightened bond purchasing which was used to stimulate growth post-covid. The Eurozone is behind the U.S. in the tightening cycle.

- The period of economic slow-down in the Eurozone is expected to last longer, however, the ECB is limited as to how aggressive it can raise rates given the fragile economic environment and the low interest rate levels that currently exist. Short-term AAA rated bonds in Europe still have negative interest rates.

FIXED INCOME

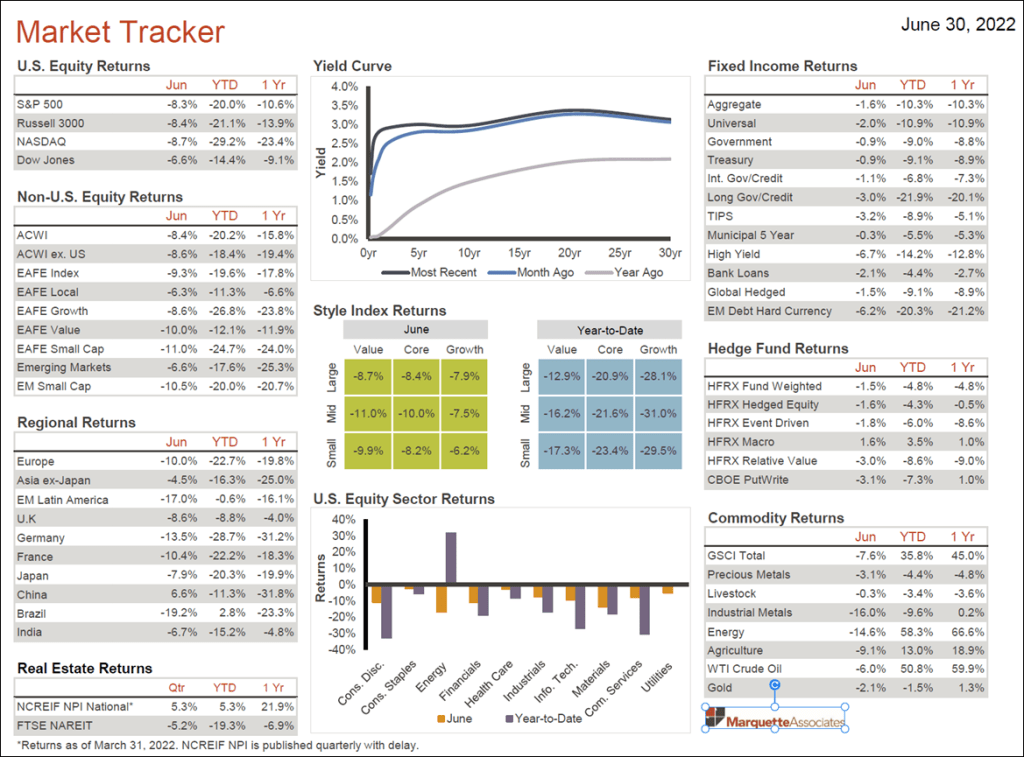

- Fixed income investments lost value in June as long-term rates on government bonds peaked mid-month and dropped precipitously to end the month slightly higher than it started. (See the Market Tracker below.)

- Corporate bonds, especially high yield, were down more because indications of a slower economy near-term negatively affected the outlook of the credit strength of corporate balance sheets.

- Inflation protected securities were negative in June because of rising interest rates whose intended purpose is to lower inflation. Upon the outlook of lower inflation in the future, inflation protected securities lost value.

- Over the last year, and year-to-date the U.S. aggregate bond index has returned a negative 10.3% return. This is one of the worst performance periods on records as a result of rapidly rising interest rates over the past year.

- It appears that long-term Treasury rates may have peaked in June 2022, but it is too soon to tell. The yield curve inverted in late June as the yield on the 2-Year Treasury at 3.10% is now higher the yield on the 10-Year Treasury Bond, just under 3%.

- Also, after the Federal Reserve Chairman spoke in early July, the interest rate outlook for Central Bank tightening was reduced from an expected peak of 4.08% in July 2023 to 3.26% in February 2023. This is a significant forecast change based on less hawkish narrative from the Fed.

EQUITIES

- Year-to-date performance of the S&P 500 Stock Index (H1-2022) was down 20%, after a significantly down month in June, as a result of the May inflation report that showed the annual inflation rate in the U.S. unexpectedly accelerated to 8.6%, the highest since December of 1981 and compared to market forecasts of 8.3%. (June inflation data is to be published on July 13.)

- The Fed immediately responded to the higher-than-expected inflation rate by raising short-term rates by 0.75%, instead of 0.50% as planned. This major turn of events led to a big sell off in stocks driving equities into bear-market territory of -20% or more.

- The stock market tumble occurred at the same time long-term interest rates were peaking mid-month. These were not good days for most investors who experienced significant losses on both stocks and bonds held in their investment portfolios.

- Toward the ladder part of the month of June the stock markets rebounded slightly to end in a loss position after a very volatile month, quarter, and half of the year.

- An unexpected development was that growth stocks outperformed value stocks (and were down less) in June. This is likely due to indication of an interest rate peak in mid-June and anticipation which would eventually enable growth firms to borrow at lower interest rates. Also, some tech stocks have been reduced in price so much that they are now listed as value stocks and not reported in the growth category.

- A severe recession would be bad for almost all equities. A severe recession in the U.S. is not likely as corporate balance sheets, employment data, and consumer spending are strong. Inflation is expected to moderate by year-end as short-term interest rate increases work through the system.

- The roller coaster will likely continue as earnings reports the rest of the year may not look so good compared to 2021 (year-over-year) when the economy, companies, and stock prices were booming.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.