U.S. Economic and Market Highlights

THE ECONOMY

- In 2022, the economy has essentially the opposite problem that it had following the 2008 financial crisis. In 2008, demand was too weak, there weren’t enough jobs to go around, and deflation was the major risk. In 2022, the economy is overheating, there is too much money chasing too few goods, and there are more jobs on offer than there are workers to fill them. This economic environment, along with war and geo-political tensions, has driven inflation to recent decade highs.

- Consumer price increases in the Eurozone region failed to moderate in July. The flash consumer price index came in at a new record high of 8.9% year-over-year, up from 8.6% in June. The consensus forecast in the U.S. is for a slightly lower year-over-year CPI rate of 8.9% in July versus the record high 9.1% rate in June.

- The balancing act for Central Banks is to raise rates enough to reduce inflation by slowing the pace of price increases while not slowing economic growth too much thus causing a recessionary environment leading to excessive unemployment.

- The European Central Bank increased borrowing costs for the first time in more than a decade in July raising rates 0.50%. The Federal Reserve raised rates in July by 0.75% which is the fourth hike in 2022 for a combined 2.25 percentage borrowing rate increase.

- All eyes are on the CPI data to see what impact the interest rate hikes are having on inflation. The next CPI report in the U.S. is on August 10 to report July data.

- Inflation expectations have dropped. Short-term TIPS (Treasury Inflation-Protected Securities) breakeven inflation rates have fallen to around 3% from a peak of 5% in late March. Longer-term breakeven rates are back in the mid–2% range.

- The International Monetary Fund revised its expectations for growth in the world economy downward. The IMF predicts global GDP to increase 3.2% in 2022 and 2.9% in 2023. Compared with the IMF’s April prediction that is lower by 0.4 and 0.7 percentage points, respectively.

- An impact of the rapidly rising borrowing/interest rates in the U.S. is the US dollar and the Euro are trading around parity. The USD and the Euro have not traded at parity since 2002. Increased interest rates and relative value of the USD also increases the borrowing costs for servicing USD debt which has a negative impact on other countries with developing markets and advanced economies.

FIXED INCOME

- With Central Bank hikes in progress and some signs of slowing economic growth, the yields on short-term rates (2-year note) are higher than long-term rates (10-year bond), thus creating an inverted yield curve scenario. A prolonged inverted yield curve is an indication of pending economic recession.

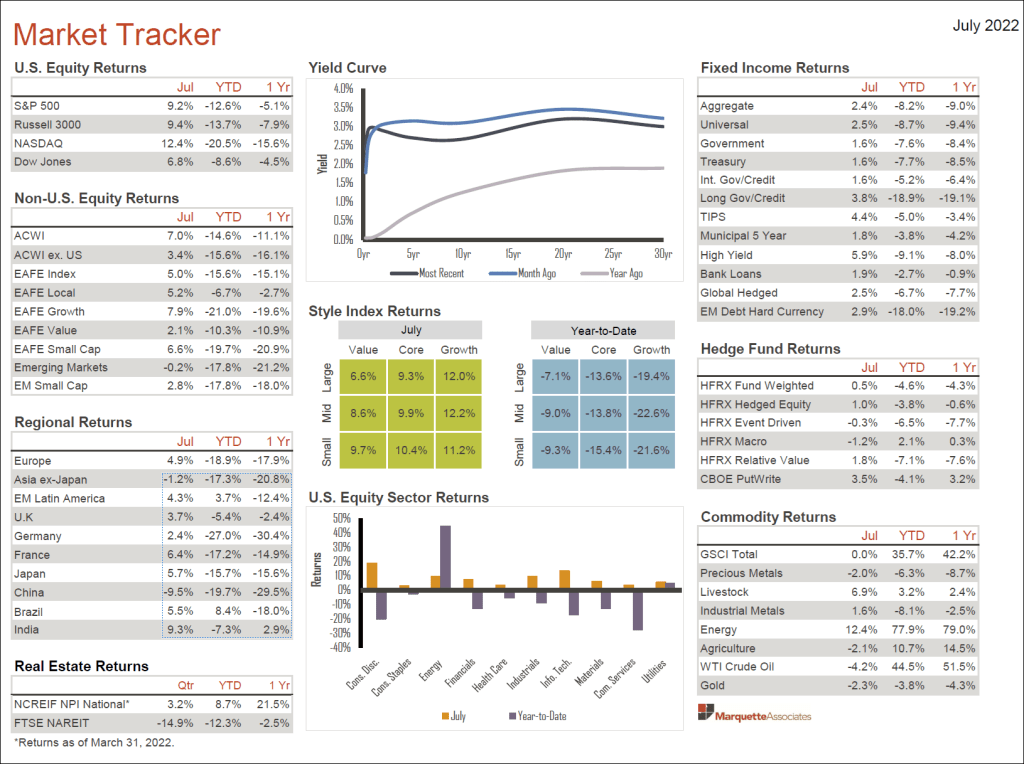

- The 10-year U.S. Treasury Bond yield declined from 3.48% on June 15 to 2.64% on July 29 which is a significant move resulting in higher market values for longer-term bonds (as market values of equivalent maturity-dated bonds move in the opposite direction of interest rates).

- Declining yields on long-term bonds resulted in a positive return for the aggregate bond index of 2.4% in July, after double-digit negative returns year-to-date on fixed income investments ending June 30. (See Market Tracker below.)

- The reason for the decreasing yields for long-dated bonds is that investors expect the Fed to stop raising short-term interest rates by year-end 2022, and start lowering rates in 2023 to reverse the expected impact of the slower economy brought on be the current rate hikes. It is a delicate balancing act that is being played out at the end of the business cycle.

- Bonds started to behave again as a stable hedge to equities after spending most of the year highly correlated with risk assets. Signs of a weaker economy ahead are likely to validate the role of bonds as a portfolio diversifier.

- Investment grade and high yield bond spreads widened as market values declined over the first half of the year. Interest rates are at higher levels creating opportunities for price appreciation on high quality bonds with low default rates. Lower rated bonds may be subject to recessionary risks as the economy slows.

- Green bonds have generally held their premium pricing structures referred to as a “greenium” (at a reduced level) because of a lower number of issuances in a rising rate environment in 2022, greater scrutiny from regulators, and a growing universe of long-term investors.

- Green, Social, Sustainable and Sustainability-linked (GSSS) bonds rose as a percentage of total global bond issuance from roughly 2% at the start of 2018 to a peak of over 12% at the end of 2021. Moody’s is forecasting that global issuance of Green bonds will be around $1 trillion in 2022, down from its initial forecast of $1.35 trillion.

- Russia’s invasion of Ukraine has rattled energy markets and led to governments fretting about energy security. The importance placed on energy security has meant that the green push from governments has been disrupted, at least in the short term.

EQUITIES

- July 2022 was the best month for the S&P 500 Stock index since November 2020, with the leading index jumping 9.2% amidst economic uncertainty.

- The reversal of recent declines in stock prices comes at a time when rate hikes are underway, and the actual impact of the Fed’s monetary action may still not be visible in companies’ earnings. Nearly three out of four S&P 500 companies have reported results beating analyst estimates which are sending signals that corporations are better placed to weather the inflation and rate hike impact.

- Investors purchase a company’s stock (or common shares) because they believe the value will rise in the future. Hopefully, this belief is supported by credible evidence and estimates about what to expect. Equity investors were more optimistic in July for several reasons.

- U.S. employers in June added a healthy 372,000 jobs, which was considerably stronger than the 265,000 expected by most economists.

- The Supply Chain Pressure Index was at its lowest level in June not seen since March 2021, meaning supply chains are loosening.

- Gas prices fell on West Texas Crude (WTC) from $122.71 in June to $98.62 at the end of July per barrel, taking off some inflationary pressure along with increased interest rates.

- There are still reasons to be cautious about buying stocks during this time of high uncertainty as Central Banks try to tame inflation without pushing the economy into a prolonged recession.

- Consumer confidence fell in July on signs of slowing economic growth, lingering high inflation, less optimism about labor markets in the near future, and concerns about their own short-term financial prospects.

- Price/Earnings (PE) Ratio on S&P 500 companies is 30.6 at the end of July, which is 52% above the average of 19.6, suggesting that the market is overvalued.

- Second quarter GDP in the U.S. decreased by 0.9%, which followed a first quarter decrease of 1.6%pushing the U.S. economy into a technical recession with two consecutive negative quarters.

- During the recession phase of the business cycle, income and employment decline; stock prices fall, and other risk assets fall, as companies struggle to sustain profitability.

- Europe experienced a stock market rally in July but continues to face great uncertainties about the outcome of the war resulting from Russia’s invasion of Ukraine and energy shortages and energy prices as the calendar moves toward the winter season.

- The Chinese stock market lost an additional 10% in July as the government renewed its crackdown on the tech sector, escalated threats to engulf the assets of property developers, and experienced a rebound in Covid-19 cases amidst further zero tolerance policies.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.