U.S. Economic and Market Highlights

Ukraine Crisis

- Last Friday was the 100th day of the war in Ukraine with Russia. Circumstances remain uncertain as Ukraine thwarts threats from the invading forces. Uncertainty persists in the region and the world regarding the long-term impact of sanctions, blockades, future energy and food sources, and price stability.

- The crisis has inflicted an extraordinary toll on the lives and livelihoods of the Ukrainian people. Approximately 20% of the population of Ukraine has been displaced. As in most crises, the vulnerable suffer the most.

- So far, foreign businesses with operations in Ukraine and Russia have managed through the disruption. Only 7% of European banks have direct loan exposure to Russian companies with banks in Italy, France, and Austria having the largest exposure.

- Seventy-percent of 281 Fortune 500 companies have either exited Russia or significantly scaled-back operations in Russia since the invasion.

- The threats from Russian officials for the use of nuclear weapons in retaliation for western countries support of Ukraine are being taken seriously by world leaders. Russia’s threats are likely to remain as such. The rising concern is that a weak nuclear-armed State is more dangerous than a strong one.

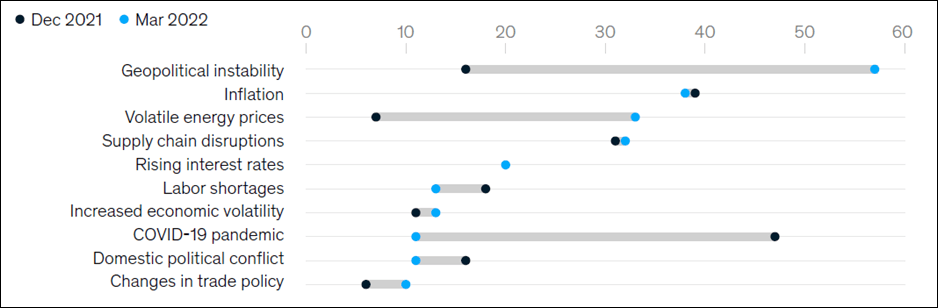

- The chart below shows the changes in respondent participants to a McKinsey survey on the Top 10 potential risks to growth in the global economy comparing sentiment in Dec. 2021 (Covid crisis) versus March 2022 (Ukraine crisis). Current concerns leading the way are geopolitical instability, volatile energy prices, and rising interest rates.

The Economy

- Central and Eastern Europe has shown surprising resilience. GDP is positive, inflation is high, and Central Banks are likely to continue raising rates with few exceptions.

- Poland increased fiscal stimulus to accommodate Ukrainian refugees resulting in increased demand for investments and consumption. GDP is estimated to average 4.7% in 2022. The National Bank of Poland is raising rates aggressively to slow inflation, which is providing support for the złoty, local currency.

- Hungary’s central bank is expected to continue to gradually increase interest rates as inflation rises due to the oil embargo, supply chain constraints, and labor shortages.

- Romania’s reported GDP was strong in the first quarter at 5.2% while pressure is being put on the government to increase the fiscal budget to accommodate higher wages and pension benefits to try to keep up with inflation.

- Czech Republic saw an upward revision in its first quarter GDP numbers leading the central bank to change/reduce the outlook for interest rates and lower the risk of a recession.

- Asian consumers are generally optimistic about the economy, expecting higher incomes and spending as consumer behaviors and finances gradually recover to normal, based on a recent McKinsey survey including consumers in India, Indonesia, Philippines, Australia, New Zealand, Japan, and S. Korea.

- As of June 1, China lifted its Covid lock-down in Shanghai. Some factories were allowed to operate during the lock-downs, resulting in a smaller contraction in manufacturing activity compared to the service sector. Forecasted GDP has been revised to 3.6% for the year.

- The US economy added more jobs than expected in May. With nearly two job vacancies available for every unemployed American the numbers would be even stronger if there was a better supply of workers. This is both a constraint on growth while contributing to ongoing elevated inflation via higher wages.

- The Purchasing Managers’ Index (PMI) indicates prevailing direction of economic trends in the manufacturing and service sectors. The U.S. preliminary PMI index fell from 56.0 to 53.8 in May, signaling a slower expansion in business activity, likely due to higher interest rates. A PMI index over 50 represents growth or expansion.

Fixed Income

- The Fed is still expected to raise rate 0.50% (50 bps) in June and July to slow the elevated pace of inflation. Capital market jitters include the concern that the Fed will overdue their rate increases and push the economy into recession.

- The European Central Bank (ECB) generally lags the Fed on central bank actions and now has additional factors to consider given the regional impact from the war and sanctions in Ukraine and Russia, respectively. A 50 – 100 bp rate hike by the ECB is expected by the end of the year, or sooner.

- The U.S. 10-Year Treasury Bond rate rose from 1.51% to 3.05% from December 31 to early June, and the German 10-Year Bund rate rose from a negative rate to 1.33 from March 4 in early June. The year-to-date performance for long-dated bonds in the U.S. and Germany were -11.1% and -9.5%, respectively, as prices on previously issued bonds fall when rates rise.

- U.S. investment-grade corporate bonds outperformed government-issued Treasury Bonds resulting in a positive performance in May for the first month this year. Investment grade corporate bond values rose (as spreads tightened) because of a slow-down in new issuances in response to a slightly lower revision to the inflation outlook.

- U.S. corporate high yield bonds also saw prices rise in May as yields fell reflecting a low number of new issuances. Companies are waiting for rates to normalize before issuing bonds in an effort to avoid setting rates on corporate debt at higher levels.

- Real Estate is one of the few asset classes, besides commodities, that has positive returns year-to-date. Inflation and rising interest rates often have a positive impact on real estate funds because owners, managers, and lenders are able to increase rental prices and interest rates thus improving cash flow results over those produced during non-inflationary periods. Also, retail and hotel sectors are recovering, post-covid, which increases the property owners’ future income.

Equity

- Thanks to the one-week rebound, toward the end of the month, the S&P 500 index posted a very small gain in May, after being down earlier in the month and remaining deeply in the red YTD. (See Market Tracker below).

- Operating margins/profits remained higher than average in the first quarter. Although,companies forecast higher costs and admitted their “limitation” to pass them along to consumers.

- Companies are increasing capital expenditures post-covid, employment remains high, and consumer spending continues to be stable although consumer confidence recently dipped.

- The current S&P 500 Price/Earnings (PE) ratio is higher than average over the last ten years. This can be explained in part by the lower-than-average earnings growth in Q1-2022 attributed to both a difficult comparison to unusually high earnings growth in Q1-2021 and continuing macroeconomic headwinds.

- Value companies (e.g., energy, utilities, and financial sectors) outperformed growth companies (e.g., technology, communications, and consumer discretionary) again in May.

- Equity returns were positive in May in Europe, Asia (except India), and especially in Latin America and Brazil measured in USD. Current equity prices are lower in European and emerging market companies generating opportunities for appreciation as countries emerge from covid restrictions. Also, energy, food, and commodity exporters have benefitted from rising prices due to inflation.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.