U.S. Economic and Market Highlights

The Economy

- The Federal Reserve policymakers raised short term interest rates in early May by 0.50% (50 basis points) as part of their effort to tamp down inflationary pressures. Additional rate increases are expected in June and July as they try to balance the risk of economic slowdown caused by higher borrowing rates.

- The risk of stagflation (high inflation and slow economic growth at the same time) is mitigated by strong U.S. domestic demand for products and services that allow businesses to pass along higher energy, commodity, labor, and supply chain-related costs onto their customers.

- The European Central Bank (ECB) announced the likelihood that it will raise rates in the third quarter. Uncertainty surrounding the current economic outlook in Europe remains high. Therefore, rate hikes may be delayed and limited until there is more clarity on the impact of the war and future inflation trends.

- One of the results of the timing difference between the Fed and the ECB is a stronger U.S. Dollar. The USD exchange rate rose by 5% compared to the Euro in April. This trend has continued as the relative value of the USD grows globally. The slowdown in China due to Covid lockdowns, the war in Ukraine, and sell-off of emerging market investments have all supported the trend toward a stronger USD.

- A negative U.S. GDP estimate for the first quarter was released based on preliminary data. The negative GDP estimate was caused by a drop in exports because of weak foreign demand due to Covid restrictions and a surge in imports, backed by a stronger USD, which subtracted significantly from GDP growth.

- In the U.S., incomes are rising, employment data improving, savings rates are high, and consumers are spending (even with higher inflation). However, continuing inflation trends, higher interest rates, and slower growth in Europe, China, and other countries will likely lessen the economic growth in the U.S.

- April’s year-over-year CPI reading marked a slightly slower pace than in March but remained near a 40-year high. But crude oil prices climbed in May to eclipse $110 per barrel. Core CPI, which excludes food and energy, increased 6.2% year over year in April.

Fixed Income

- So far in 2022, returns from fixed income investments (bonds) have been significantly negative with the Bloomberg Barclays Aggregate Index declining almost 10% YTD at the end of April. (See market tracker below.)

- Unlike more risky assets like stocks or high-yield bonds, a quarterly loss of more than 5 percent in the high-quality fixed income space is very rare. The 10-year U.S. Treasury Bond yield rose above 3% and remains volatile.

- With investors’ focus on the Fed’s commitment to raising interest rates multiple times to slow down inflation, current market prices on bonds have built-in multiple rate increases. The impact has been significant on bond prices since interest rates had come from such a low starting point (during the covid crisis).

- Counterintuitively, rates at the longer end of the Treasury curve usually peak at or near the beginning of a Fed-rate-hiking cycle. So, the probability of a continued decline in high quality fixed income investment values is less likely moving forward in the business cycle.

- It is also helpful to remember that high quality bonds are contractually redeemable at par ($100) on their maturity date, regardless of what happens to the price during the term of the bond. The coupon rate may state a lower rate than the compounded internal rate of return (IRR) paid out on a bond at maturity. A higher IRR closes the gap as the discounted bond value proceeds toward its issued par value.

- For investors with longer-term investment time horizons and higher risk tolerance, below investment grade securities (e.g., high yield corporate bonds), floating rate bank loans, and securitized assets (e.g., mortgage-backed securities) may be preferred because of their higher yields, credit risk diversification, and reduced impact from government bond yields.

- The U.S. imposed a broad range of severe sanctions on Russia after its invasion of Ukraine. Sovereign and corporate bonds from both countries are under stress. Russia’s bonds are trading at distressed levels and have been ejected from the bond market indices. Ukraine’s bond issuances have shrunk within the USD index/market and is on hold in the local currency index.

US Equity

- As of mid- May, the Dow Jones Industrial Average endured its seventh consecutive weekly loss and the S&P 500 stock index declined further toward a bear market set back. A bear market is when stock prices fall 20% or more for a sustained period.

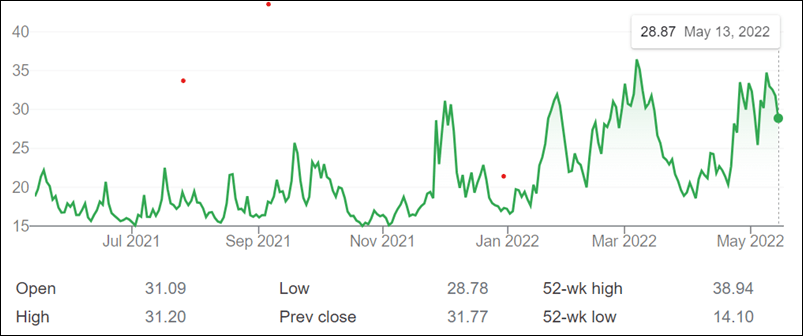

- High volatility is back in May after a short reprise in April. The chart below shows the CBOE Volatility Index over the last year.

- Volatility is measured by the standard deviation of a stock’s annualized returns over a given period and shows the range in which its price may increase or decrease. The approximate long-term average volatility for large-cap stocks, aggregate bonds, and cash are 17%, 4%, and 0% respectively.

- Short-term market volatility is unsettling, but historically not unusual. Diversified portfolios in alignment with the investor’s time horizon and risk tolerance, generally experience a divergence of returns and volatility that smooth out over time, turning short-term corrections into temporary deviations in a long-term investment plan.

- There have been 26 bear markets in the S&P 500 Index since 1928. There have also been 27 bull markets—and stocks have risen significantly over the long term. Bear markets tend to be short-lived. The average length of a bear market is 289 days, or about 9.6 months.

- U.S. companies reported single-digit earnings growth (profits) for the first time since Q4 2020. The lower earnings growth rate for Q1 2022 relative to recent quarters can be attributed to both a difficult comparison to unusually high profits in Q1 2021 and continuing macroeconomic headwinds (e.g., inflation and supply-chain shortages).

- Analysts predict a single digit earnings growth rate (profits) in Q2 and a strong second half of the year in the U.S. ending with double-digit profits for the year. The Services sectors have been the largest contributors to the increase in profits so far in the second quarter.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.