U.S. Economic and Market Highlights

The Economy

- Sanctions by allied countries in response to Russia’s aggression for its baseless war against Ukraine have further exacerbated strained supply chains and caused energy prices to sharply rise.

- The Consumer Price Index (CPI) reached a four-decade high in the U.S., rising 7.9% year-over-year in February driven by increases in gas, shelter, and food. Core inflation (excluding gas and food) rose to 6.4%. Wages have also risen, but not at the pace of headline inflation.

- The Eurozone has closer economic ties with Ukraine and Russia, particularly when it comes to reliance on Russian oil and gas for a primary source of energy. Estimates show that inflation was up to 7.5% in March.

- The European Commission announced a plan – RePowerEU – designed to diversify sources of gas and speed up the roll-out of renewable energy. However, in the meantime there are fears that the high energy prices will weigh on both business and consumer demand, hitting economic activity.

- Record high inflation prompted the Federal Reserve to raise short-term interest rates 25 basis points (bp) (0.25%) in March and announce a more aggressive stance toward fighting inflation. Revised expectations from analysts have built in the possibility of a 50 bp hike in May and another 50 bps in June.

- The European Central Bank (ECB) outlined plans to end bond purchases and indicated that a first interest rate rise could potentially come this year.

- The world GDP growth forecast for 2022 was revised downward by 0.7 to 3.5%, with the eurozone cut by 1.5 to 3.0% and the U.S. by 0.2 to 3.5%. This reflects the drag from higher energy prices but also a faster pace of US interest rate hikes than previously anticipated. The world growth rate for 2023 was revised down by 0.2 to 2.8%.

- The labor market in the U.S. continues to normalize as participation rates increase to pre-Covid norms. The unemployment rate fell to 3.6% in March.

In Europe the average unemployment rate fell to 6.2% in February ranging from Germany at 3.1% and Spain at 12.6%.

- Private commercial business investments are still projected to be strong in 2022. In the U.S. manufacturing firms intend to increase capital expenditures by 7.7% and service companies anticipate a 10.3% increase. In the eurozone the composite purchasing managers’ index (PMI) was 54.5 in March (slightly down from February) but over 50 which represents expansion.

Fixed Income

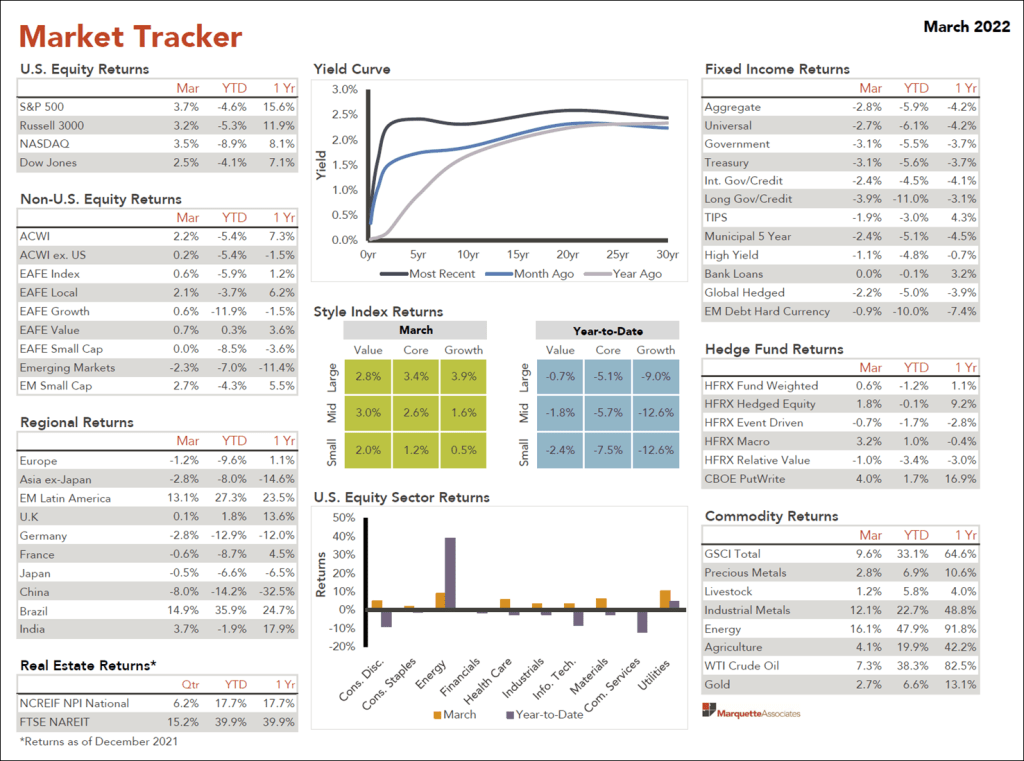

- Bond yields have risen sharply across the yield curve in 2022 (e.g., 10-year Treasury Yield rose to nearly 2.8% from 1.5% at the end of 2021).

- As rates rise, bond prices fall. The Bloomberg U.S. Aggregate Bond Index was down 5.9% for the quarter and the Global Aggregate Index suffered its biggest decline from a peak in data going back to 1990, surpassing the losses experienced during the financial crisis in 2008.

- With cheaper bond prices, more attractive purchasing opportunities exist. As current bonds mature, new bonds will be available for purchase that pay higher interest rates.

- Examples of bond issuances that are increasingly popular, especially in Euro-denominated markets, include Green Bonds, Sustainability-linked, and other ESG* issuances. The limited history of these bonds shows great promise for competitive rates and adequate liquidity with the bonus of increased ESG responsibility. Other countries are initiating similar investments including Poland, Chile, Indonesia, and the U.S.

* Environmental, Social, and Governance

- ESG bond issuances span various industry sectors and include maturities all the way out to 30 years, with the 10-year bond being the most popular. The ESG bond market will likely increase in size as the U.S. Securities and Exchange Commission ESG disclosure requirements increase in the coming years.

Equity

- Global stock markets finished down for the quarter but posted the first positive month for the year in March 2022. The S&P 500 Index was down -4.6% for the quarter, marking the first time in two years the index was down for a quarter. The index was up 3.4% for the month of March. (See the Market Tracker below.)

- Stock markets exhibit a defensive tone as income related, and value-style, sectors fare best (e.g. real estate, utilities, and consumer staples), while Growth stocks remain under pressure as investors reassess their valuations in light of expected higher interest rates.

- Global equity volatility (mostly negative) continues into April as investor sell shares in the face of increased uncertainty resulting from the Russia Ukraine conflict and rapidly rising interest rates. Emerging market equities in Latin America and Brazil started the year strong after disappointing results in 2021.

- Russia and Ukraine account for 30% of global wheat exports and over 25% of fertilizer exports. Agriculture is the largest part of Ukraine’s economy, accounting for 14% of its GDP. Farmers in many countries are under pressure because of a reduced supply, and higher prices, for fertilizer during the planting season.

- Allied Sanctions have focuses on Russian gas and oil and the Russian financial system. Assets of the Russian Central Bank were frozen, Russia’s access to the global financial system was stalled, some of Russia’s wealthiest people have also been hit with asset freezes and seizures, while a slew of major international corporations have withdrawn from the country. Numerous other sanctions have been instated.

- Russia was removed from equity indices effective March 2022 as part of sanctions related to Putin’s invasion of Ukraine. More than 4 million Ukrainian citizens have been forced to flee the country according to the United Nations. The exodus is the largest movement of people in Europe since World War II. Casualties on both sides in the thousands and over 1,000 civilian deaths.

We continue to urgently pray for peace.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.