U.S. Economic and Market Highlights

The Economy

- The tragic events of Russia’s invasion of Ukraine have created a humanitarian crisis and devastating loss of lives and property. We pray urgently for peace!

- As the war continues, the level of economic uncertainty increases, especially in eastern Europe. With increased sanctions and elevated prices on commodities, the risk of stagflation in Europe continues to build.

- Stagflation refers to an economy with limited growth and higher than normal inflation. Most commodities have nearly doubled in price in recent weeks, including coffee, lumber, natural gas, and crude oil which touched $130 a barrel, hitting a 13-year high.

- These rising prices are expected to prompt Central Banks to raise rates to attempt to control the further increase in prices. By tightening interest rates they hope to slow economic growth which was on the trajectory of record high levels due to the Covid-19 recovery.

- Now, Central Banks will have to be more cautious with the timing and frequency of rate hikes because of the increased risk of slowing too much the economic growth balance into recession.

- The war has elevated the risk of higher inflation and slower growth precipitously by at least 1% higher inflation and 1% lower growth, than the above average growth rates previously projected for 2022, less than a month ago.

- The crisis has impacted the currency markets around the world, especially in Europe, where the Euro is trading below 1.10 against the USD and the Russian Ruble is now worth less than a penny after falling more than 30% last week.

Fixed Income

- With the increased uncertainty, capital markets have reverted to a “risk-off” mentality moving money to government bonds to preserve principal. Consequently, the rates on long-term government bonds declined as prices rose.

- The U.S. Treasury 10-year bond yield dropped over 30 bps from over 2% in mid-February to 1.70% in early March, while the E.U. 10-year government bond yield dropped from +0.30% in February before the invasion to -0.028% in early March.

- The result of higher short-term interest rates and lower long-term interest rates is a flattening of the yield curve (when rates on bonds are nearly the same regardless of the maturity terms). When short-term yields rise above long-term rates, the yield curve becomes inverted, which is usually considered bad news for the short-term economic outlook as it has been a predictor some previous recessions.

- As government bond values have risen, corporate bonds have sold off. This has created limited buying opportunities. Investors remain cautious, amidst the uncertainty, and may not jump back into the risk-on mindset until the fog of war has cleared somewhat. In the meantime, opportunities may exist for high quality corporate bonds and government agency mortgage-backed securities that have dropped in price.

Equities

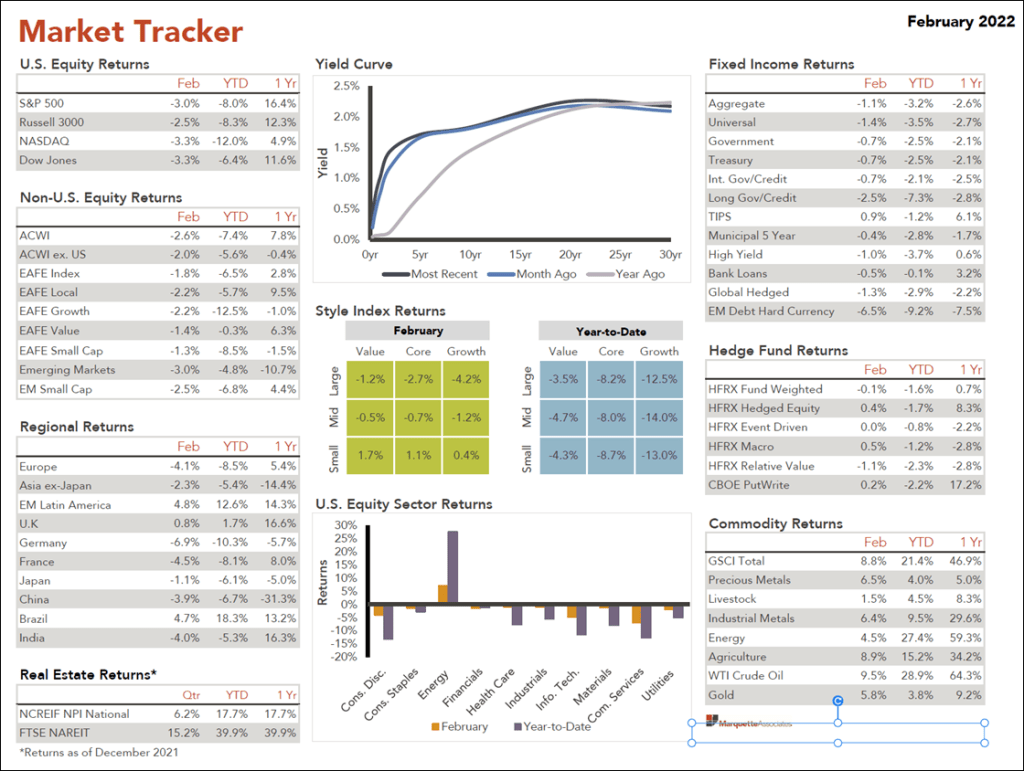

- The above-mentioned concerns have led to an official stock market correction of more than a 10% decline from market highs in early January. (See Market Tracker below.)

- Company stock owners are concerned that higher oil prices may negatively impact earnings in the first quarter and slow economic growth in 2022. Energy companies have been the only sector to have consistently positive returns since the war broke out.

- Positive economic reports are expected out this week showing the durable goods spending was up in January and February, as the Omicron outbreak had less of an impact than what was expected. However, the percentage increase in spending was significantly lower than the peak reached in March 2021.

- Disposable income and savings rates in the U.S. were down in January and February as government support programs expired.

- These data patterns, when applied to anticipated “pre-war” inflation trends, show that inflationary pressures caused by economic stimulation, recovery, and supply chain shortages were on the decline.

- Recent economic data from the E.U. showed recovery and reasons for optimism. Emerging markets anticipated a slightly slower recovery rate from the pandemic due to higher covid-cases, higher commodity prices, and higher interest rates.

- The outbreak of war in eastern Europe has stalled, if not stopped, the positive outlook for economic recovery in 2022 and put the world in a state of shock over the harm and sadness created by the Russian invasion of Ukraine.

- We pray urgently for peace!

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.