U.S. Economic and Market Highlights

The Economy

- Economic growth and earnings growth were positive in the fourth quarter and are expected to continue into 2022, albeit tempered by more modest growth than what was experienced during the initial stages of the (post) Covid 19 economic recovery.

- U.S. jobs grew more than expected to start the year and sizeable revisions to previous month’s Labor Department reports sent payroll gains almost 3-times higher. Encouragingly, many of the additional jobs were in leisure and hospitality sectors and the labor force participation rate rose to 62.2%, the highest level since the pandemic started.

- Central Banks are taking action to contain inflation as upward pressure on prices continue. One example of rising prices is the West Texas Intermediate (WTI) crude oil futures price which passed $92 per barrel this week, the highest level since August 2014.

- The U.S. FED is wrapping up its tapering of bond purchases and indicated multiple interest rate hikes coming over the next year. The U.K. BOE raised rates for the second time in as many months by an additional 25 basis points, and the E.U. ECB announced this week that it is no longer ruling out an interest-rate hike this year.

Fixed Income

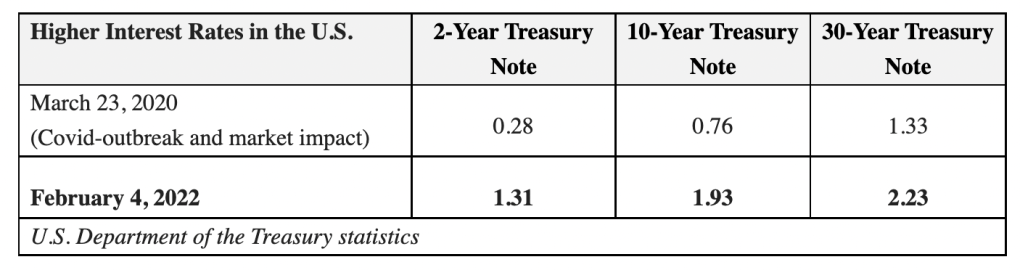

- After a gradual rise over 18+ months since the outbreak of Covid, rising interest rates gained momentum since the start of the year. As a result, bond prices fell further with the optimistic payroll reports and continuing inflationary pressure.

- Interest rates are trending higher in most countries. The pace of acceleration varies based on each country’s economic situation. Mexico, Brazil, Russia, China, and the U.K. have already raised rates while the U.S. and Canada are ready to start raising anytime, and the E.U. and Japan have only recently eclipsed the zero-interest rate environment.

- Rising short term rates (are initiated by Central Banks) and cause the yield on short term deposit accounts to increase and directly impacts the interest rates charged on floating/variable rate loans.

- Rising intermediate and long term rates (are market driven) and are influenced by the demand for yield from investors. If investors require higher rates when purchasing bonds, then market values decline on current bonds held in the portfolio at lower rates.

- The forecasted yield curve in the U.S. shows that short term rates in the U.S. are expected to rise while long term rates are expected to remain somewhat stable. This of course remains to be seen, but at this point is the most likely scenario because of inflationary pressures that the Fed needs to address by hiking short term rates. On the long end of the curve, rates in the U.S. may not rise too much because growth will likely slow as the recovery from Covid 19 stabilizes and global influences such as slow growth and geopolitical concerns remain. (e.g. Russia, Ukraine, China, and Taiwan).

Equity

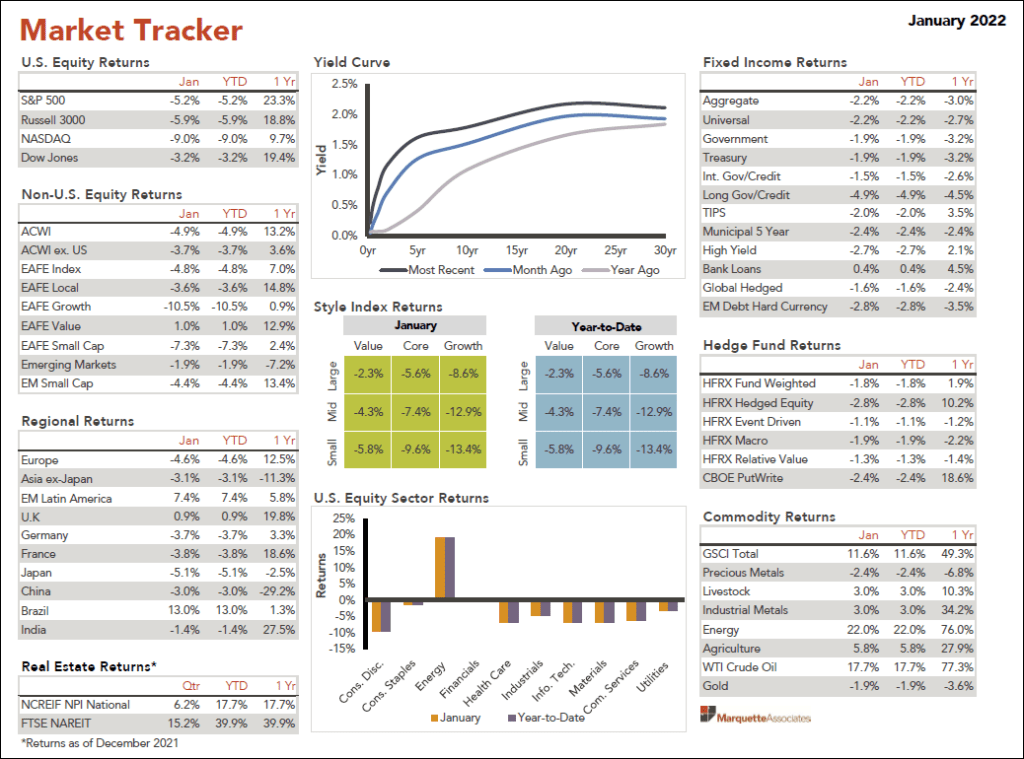

- The S&P 500 Stock Index finished 2021 near a record high. Most indices had double digit returns regardless of the component companies’ size, style, or sector concentration.

- Markets sold off in January 2022 primarily because of the hawkish stance from central bankers toward interest rate hikes. Growth stocks such as technology and internet-related companies were down the most. When interest rates rise value stocks, such as financial and energy companies generally outperform growth stocks such as technology and tele-communication companies. (See Market Tracker below.)

- The market sell off did not come as a surprise given that it has been more than 18 months since the market exhibited downward shifts after almost uninterrupted upward momentum for a year and a half.

- Over time equity returns tend to revert toward average return percentages. Over the last several years performance returns were well above average. This recent, oversized increase would generally indicate that equity performance in the near term will likely be more modest.

- As interest rates rise, the benefits of investing in stocks will likely decrease. However, historical returns are generally favorable, for equities during inflationary periods when the economy is expanding and price levels are elevated, thus serving as a hedge against inflation.

- Non U.S. developed markets (e.g. Western Europe, Canada, Australia, and Japan) outperformed emerging markets with positive earnings surprises and improved investor sentiment. Emerging markets saw the most volatility amid China’s changing regulatory landscape. China (technology) growth stocks were under pressure most of 2021 that resulted in double digit, negative returns. Most other emerging markets and smaller value oriented companies performed better than non U.S. developed markets.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.