U.S. Economic and Market Highlights

THE ECONOMY

- Unemployment rates continue to decline in most economies around the world as recovery from the pandemic gradually continues. In some cases, unemployment rates are decreasing even though jobs are not being added because of low Labor Force Participation Rates.

- The Global Labor Force Participation Rate has shown a steady decline since 1990. The Participation Rate measures the number of people who are actively seeking jobs as well as those who are currently employed.

- In the U.S. the participation rate stabilized in 2013 at 63% (down from nearly 67% a decade earlier). Since COVID-19 the participation rate dropped to nearly 60% and now resides at 61.9%. Evidence supports that many former workers who were furloughed did not return to their jobs.

- The result of lower participation rates is a scarcity of workers, under-staffed organizations, and pay pressures on employers trying to attract staff to fill vacant positions.

- Other contributing factors to labor shortages is the aging populations in most economically developed countries.

- A result of the unexpected tight labor market is higher inflation and service and production limitations. Hourly wages in the U.S. were up 4.8%, while core inflation (excluding food and fuel) was 4.9%, and headline inflation was 6.8% year-over-year.

- As inflation rates trend higher and economic recovery continues, most Central Banks have indicated a willingness toward more hawkish monetary policies, including less government stimulus and potential for short-term interest rate hikes.

FIXED INCOME

- In anticipation of higher inflation and tightening monetary policy, the 10-Year U.S. Treasury Bond yield rose more than 0.25% (25 basis points) since the beginning of the year to nearly 1.80%. The 10-Year Eurozone Central Government Bond yield also rose approximately 25 bps since the beginning of the year to a positive 0.36%.

- As government bond yields rise market values generally decline on previously purchased bonds with lower interest rates. Over time, as current low interest rate bonds mature and higher interest rate bonds are purchased, yields from fixed income investments will improve.

- Corporate investment grade and high yield bonds generally have tight credit spreads suggesting high valuations in the current interest rate environment. Corporate bond valuations are supported by higher corporate profit growth and low default rates. As rates trend higher, purchasing opportunities are likely to develop.

- Emerging market credits have not increased in price as much as developed market bonds and therefore are cheaper. However, these bonds have other risks to consider such as currency rates, liquidity, and political risks.

- Infrastructure investments continue to be resilient as funding levels increase and new commitments have been made to clean and renewable energy projects. The U.S. recently approved a $1.2 trillion infrastructure bill with specific mandates that include expansion of the clean energy transmission grid, modernization of the public transit passenger rail system, national network of electronic vehicle chargers, and fleet of zero- and low-emission school buses that will support domestic jobs and manufacturing.

EQUITIES

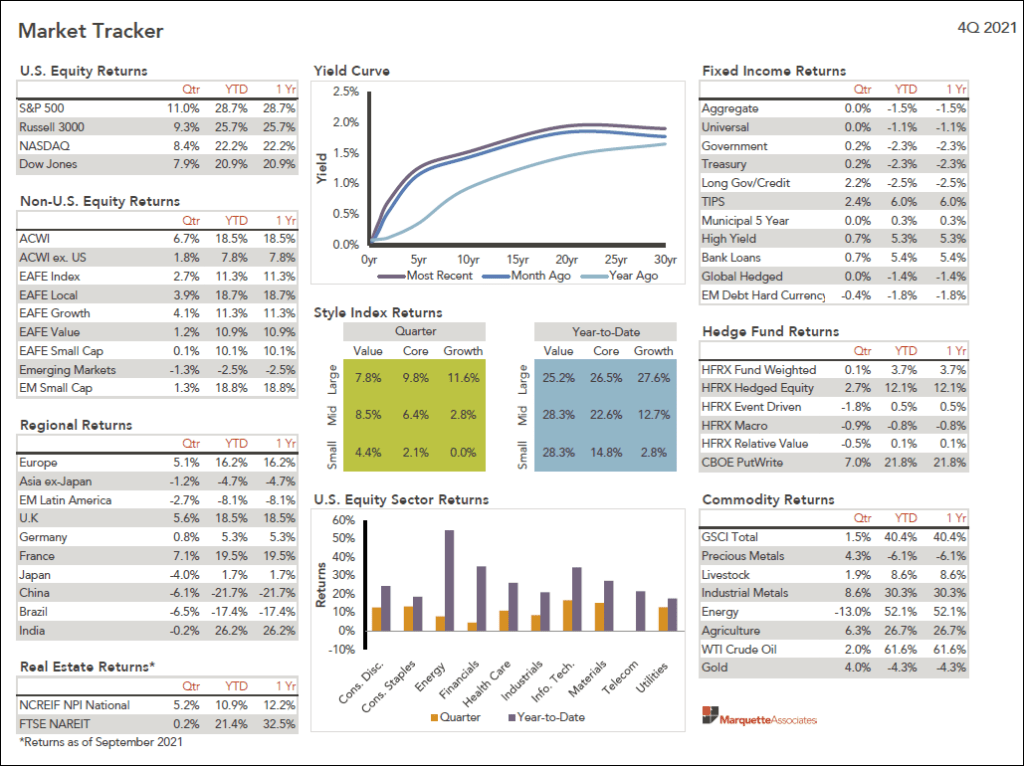

- Equities ended 2021 on a positive note with developed market indices achieving double digit returns for the year. The exceptions were the emerging markets of Latin America and Asia who had negative returns in 2021. (See the Market Tracker below).

- For the first time in a decade, value-oriented stocks (e.g. Energy and Financials) performed almost equally as well as growth stocks (i.e. Technology and Communication Services). There were strong corporate earnings reported throughout the year with few exceptions.

- The best performing sectors were Energy (+54%), Real Estate (+46%) and Financials (+35%). The weakest sectors which also had strong performance were Utilities (+18%) and consumer staples (+19%).

- The market values of large-cap U.S. companies continue to be elevated as equity indices in 2021 reached new all-time highs. Other markets such as Europe, Japan, and Emerging Market (EM) economies present lower valuations at the start of 2022.

- In the first full week of trading in the new year, equity markets were down because of increasing inflation and interest rates. These economic trends are likely to continue in the near term. Historically, inflation has not impeded diversified equity investment returns especially if it comes with economic growth.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.