U.S. Economic and Market Highlights

- The U.S. Fed has gradually raised interest rates since December 2015, and is expected to raise another 25 bps in June, in an effort to fulfill their “dual mandate” of promoting price stability and strong employment.

- Core Personal Consumption Expenditure (PCE) jumped to 1.9%, year-over-year, nearing to the Fed’s 2.0% target, and U.S. job growth increased in April and the unemployment rate dropped to a near 18-year low of 3.9% near the Fed’s forecast of 3.8% by year-end.

- Generally, market swings exaggerate during periods of rising interest rates. This pertains toGDP – which expands higher and recedes lower; Stocks – which demonstrate more marketvolatility, and Bonds – which benefit from increased yields and suffer from declining price values when rates rise.

- The opposite is being realized in the Eurozone and the U.K. where GDP grew by 0.4% and 1.2%, respectively, in the first quarter and both ECB and BOE (their Central Banks) left interest rates unchanged.

- Back in the U.S. – Six of the ten Leading Economic Indicators (LEI) made positive contributions and all 11 industry sectors reported positive earnings, in April, led by energy, financials, technology, and industrials. Many company management teams have pointed to lower taxes and strong sales growth as primary drivers of healthy profit growth.

- However, geopolitical headlines continued to weigh down stock market returns as concerns about potential trade wars increased as the Trump administration pursues steel and other tariffs impacting products from multiple nations.

- Oil prices rose 5.7% to above $72 a barrel in April amid inventory declines, expectations for continued OPEC production cuts, and uncertainty around U.S. plans for Iran and Syria.

- The yield curve steepness did not change much in April as yields on both the short and long-end of the curve climbed slightly more than 20 bps. Short-term rates supported by Fed hikes and Long-term rates supported by higher growth rates and inflation.

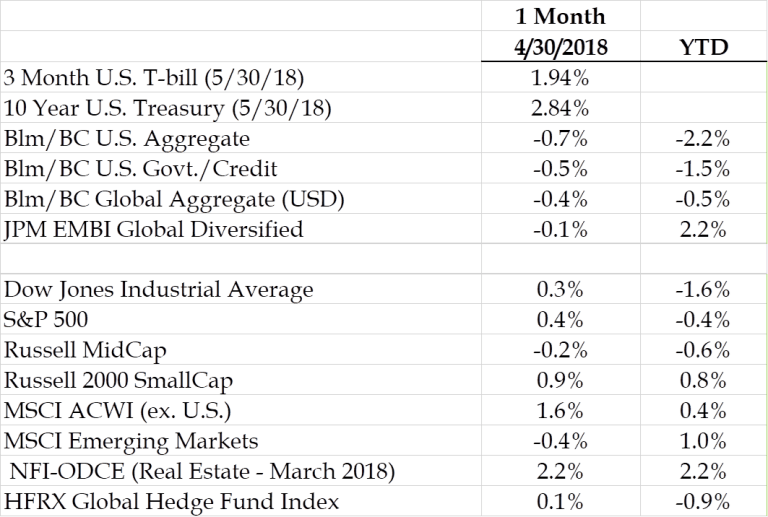

- With rising rates came negative returns on interest rate sensitive bonds – U.S. Treasuries, Agencies, and Investment Grade corporate bonds have all posted negative 12-month returns while Emerging Market bonds barely broke even over the last twelve months.

The above was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results. Analysis done in cooperation with Cedar Hill Advisors.