U.S. Economic and Market Highlights

- U.S. and developed market international stocks stumbled in the first quarter of 2018, tripped up by concerns surrounding inflation, trade policy spats, and the threat of increased regulatory focus on high-flying technology sector companies.

- Growth style U.S. stocks extended their sharp 2017 outperformance over value their peers during the quarter, as the Russell 3000 Growth Index generated a total quarterly return of 1.5% compared to the Russell 3000 Value Index’s 2.8% decline.

- Over the long-term, however, the U.S. stock market exhibited volatility on both the upside and downside. According to Morningstar data, the S&P 500 Index’s 50-year average annual return is 10.2% and its annualized standard deviation of returns over this period is 15.9%. In statistical terms, this means investors can assign a roughly 67% probability that the U.S. stock market will return between -6% and 26% in any given year.

- When volatility increases despite economic and corporate fundamental strength, often a change in sentiment occurs. In the first quarter of 2018, fundamentals remained strong. Inflation did not spike, unemployment remained at, or near, historical lows, and fourth quarter GDP growth of 2.9% was above the Federal Reserve’s long-term potential growth rate. This followed consecutive quarters of 3.0% plus growth in the summer. Skeptics may argue that markets only care about future growth rates, and thus equity market weakness suggests slower growth ahead.

- Yet, we see several important tailwinds which could support broad-based growth in 2018 including the recent U.S. tax reforms, strong corporate earnings momentum, and low interest rates across most of the world.

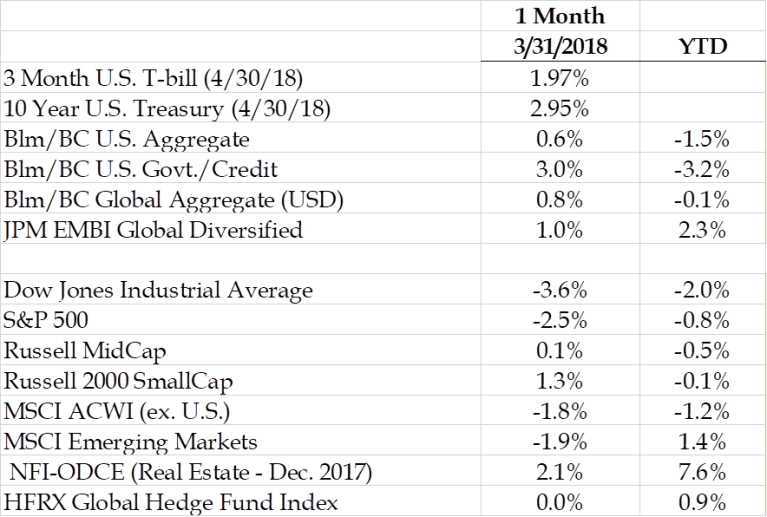

- As inflation fears persisted through February, interest ates continued to climb higher, even as first quarter GDP estimates fell. Rates declined in the second half of the quarter as inflation fears eased; yields on the benchmark 10-year U.S. Treasury bond traded down from 2.95%, to 2.74% at the end of March, and back to 2.95% at the end of April.

- Federal Reserve officials shifted toward a moderately faster pace of interest rate policy tightening at their March meeting as their growth forecast and confidence in reaching their inflation target improved.

- Historically, rising short rates have a flattening impact on the slope of the yield curve, essentially making long duration bonds less attractive relative to shorter maturity bonds. We’re seeing the same result this time around as the Fed continues to hike federal fund rates.

- Broad consumer inflation rose to 2.4% in March; the U.S. 10-year Treasury inflation breakeven rate climbed to a four-year high of 2.14% in mid-March.

- The tight labor market has also been moving wage growth higher. In March, the twelve-month increase in wages crept up to 2.7%. Although, monthly payroll additions might be smaller in 2018 than in recent years given the 17-year low 4.1% unemployment rate.

- Consumer confidence declined moderately in March after reaching an 18-year high in February. Consumer optimism could remain elevated in 2018 given the healthy job market and lower personal income tax rates for most Americans. With wages and house prices on the rise and the S&P 500 Index still roughly 12.0% higher than a year ago, it should come as no surprise that consumer confidence remains robust.

- Oil prices have significantly rebounded since the $25-$30 per barrel lows of early 2016. The closing price of a barrel of U.S. crude oil at the end of March was $64.94, nearly 28% higher than the closing price of $50.60 per barrel on March 31, 2017. Rising oil prices can have a negative impact on consumer and investor confidence.

The above was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results. Analysis done in cooperation with Cedar Hill Advisors.