U.S. Economic and Market Highlights

Amidst a stock market correction, occurring over the last couple of months, recent economic data support continued strength for moderate growth, unless outside factors interrupt recurring momentum.

- Fourth quarter GDP, in the U.S., was revised upward to 2.9%, resulting in three consecutive quarters near or above a 3% growth rate, which is above the Fed’s long-term, informal expected growth rate target of 2.5%.

- This acceleration has led to a more hawkish stance on interest rates from the Fed, as they raised the (short-term) Fed Funds rate in March to 1.75%, as U.S. job growth and unemployment rates remain very favorable.

- The other trigger for higher interest rates is higher inflation. However, so far in 2018, inflation rates have remained somewhat calm with the Personal Consumption Expenditure (PCE) index climbing at a pace of 1.8% on a year-over-year basis in February, and core PCE, (the Fed’s preferred measure excluding volatile food and energy prices), rising 1.6% on a year-over-year basis.

- From a different venue, the European Central Bank (ECB) announced that its benchmark interest rate will remain at 0.00%, and may remain there for an extended period, due to projected inflation rates of 1.4%, which is below their targeted rate of 2%.

- This divergence in the status of the economic recovery has been reflected in the stock marketprices in different markets. The current price of stocks compared to the historical average price of stocks is much higher in the U.S. (and in Emerging Markets) than it is in Developed Markets(outside the U.S.) including Europe, Australia, and Japan.

- The continuous, quarterly stock market increases in the U.S. through January 2018, along withaccelerating growth and inflation have led to concerns among some investors that the Fed will raise interest rates more aggressively than anticipated.

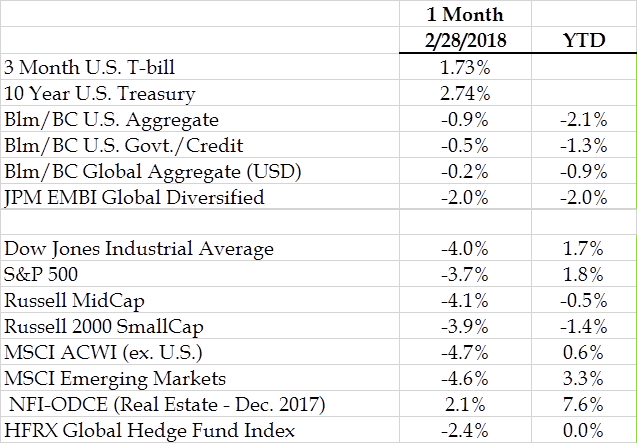

- In February and March, volatility and risk-off sentiment re-emerged and spread across globalmarkets. As of March 31, the S&P 500 fell 2.1% during the quarter, its first quarterly loss since the third quarter of 2015.

- Other factors leading to investor uncertainty were: the Trump Administration’s newly announced tariffs on Steel of 25% and Aluminum of 10% and on other Chinese products which might affect the U.S. economy and overall international trade, the U.S. recently passed a fiscal budget which will substantially increase Government borrowing and spending, and there is a new potential for increased regulation in the technology sector.

- After the recent correction in stock prices, values remain relatively high compared to historical averages. Thus, strong corporate earnings growth in 2018 and 2019 are needed to sustain increased price levels. Analysts are estimating stronger growth in 2018 earnings of year-over-year increases of over 20% in each quarter, primarily driven by the reduced corporate tax rate.

- U.S. Treasury bonds posted negative returns year to date and over the last twelve months as themarket’s recent concerns about accelerating growth and inflation have driven yields higher and prices lower thus far in 2018.

- Although signs of a flattening yield curve also exist as short-term rates rise faster than long-term rates, corporate bonds spreads widened as yields generally rose pushing bond prices down.

- Global REITs experienced an especially challenging February, as a move higher in U.S. interest rates put pressure on prices of many higher yielding sectors.

- Global private equity fundraising remains strong with a growing presence of private equity funds within Europe and Asia. While private equity valuations are high, they remain relatively attractive and do not appear overvalued when compared to the public equity markets.

The above was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy.

Past performance is not indicative of future results.