U.S. Economic and Market Highlights

- Stocks globally snapped a record 15 month winning streak and were lower in February, due tosharp selloffs at the start and end of the month. The Dow Jones industrial average lost 4.3% and the S&P 500 fell 3.9%.

- The new Fed Chair Powell recently gave an upbeat view on the U.S. economy and said the data has strengthened his confidence on inflation, which is being interpreted as a more bullish sentiment for raising interest rates than his predecessor, Chair Yellen.

- February’s correction in stocks was due to worries of rising inflation, rising interest rates, and the rising value of the U.S. Dollar. A correction is generally defined as a drawdown of 10% or more from the most recent highs.

- Since the beginning of the current bull market in March 2009, on average, corrections occur about once per year. The average decline was 11.7% and lasted 57 calendar days (about eight weeks). While corrections can be painful in the short-term, since the financial crisis they have tended to occur somewhat frequently, but have often been relatively short-lived.

- Most global economies are experiencing healthy levels of growth and the U.S. corporate sector is showing signs of strong corporate profits, while the impact of the corporate tax cut from 35% to 21% has not yet been observed in recent earnings releases.

- The University of Michigan Survey of Consumers rose in early February to its second highest level since 2004 despite stock market volatility. The reading of 99.9 was supported by rising incomes, employment growth, and a favorable perception of tax reform. The report signaled high levels of confidence in the economy among U.S. consumers.

- The Financials sector was among the top performing sectors last month, benefitting from strong earnings trends, higher interest rates, and increased credit growth. Interest rate sensitive sectors including utilities and real estate lost ground last month.

- The U.S. 10-year Treasury yield reached a 52 week high of 2.94% in February, its highest yield since January 2014, resulting in a steepening yield curve. The 30-year fixed mortgage rate rose to an average of 4.38% this week, the highest level in nearly four years.

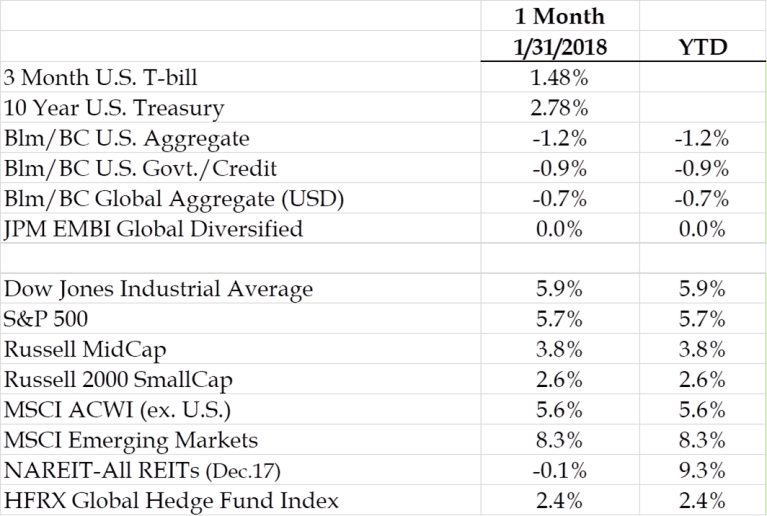

- U.S. Treasuries and Agencies posted negative returns thus far in 2018 as investors began to account for more Fed rate hikes and potentially higher levels of future inflation.

- The Core Personal Consumption Expenditure (PCE) price index rose 0.2% in December. The year over year reading for Core PCE increased 1.5%, remaining below the Fed’s 2.0% target. Headline CPI, which includes volatile food and energy costs, rose an annualized 2.1% at year end. The average hourly earnings advanced 2.9% in January from the same period one year ago marking the highest level of yearly wage growth since 2009.

- U.S. crude oil prices remained relatively high in January, climbing 7.1% to close the month at $64.73 per barrel, which is almost double the price per barrel of $33.62 in January 2016.

The above was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results. Analysis done in cooperation with Cedar Hill Advisors.