U.S. Economic and Market Highlights

The Economy

- The International Monetary Fund (IMF) lowered its 2021 global GDP growth forecast to 5.9 percent and kept its 2022 forecast unchanged at 4.9 percent.

- U.S. Consumer sentiment was slightly lower amid elevated inflation and a late summer resurgence in COVID-19 cases. However, consumer balance sheets remain quite healthy.

- Rising energy costs emerge as primary source of inflation worries. Soaring energy prices and ongoing supply chain issues have exacerbated inflation concerns.

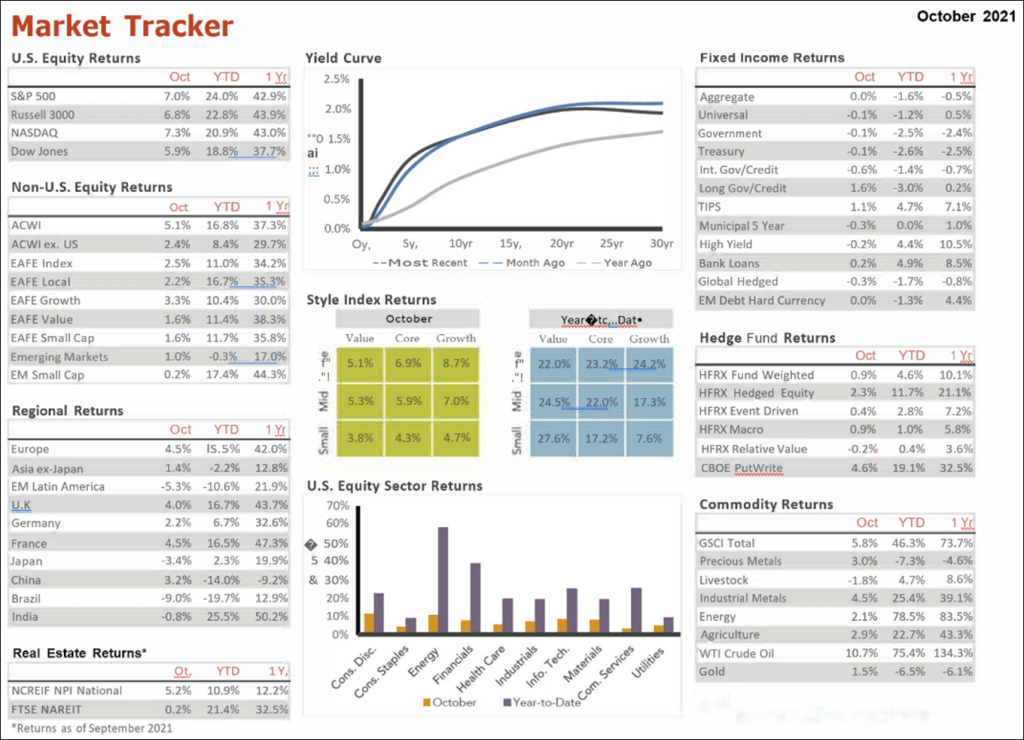

- U.S. Treasury Inflation- Protected Securities (TIPS) break-even levels estimate the average annual inflation rate over the next five years to 2.5%.

Fixed Income

- At the beginning of the 4th quarter long-term interest rates in the U.S. were trending higher.

- As interest rates rise, bond prices generally fall, especially on longer-dated bonds whose values are more likely to be eroded from inflation.

- An underweight to fixed income in multi-asset class portfolios remains common as bond returns for the year have been mostly negative and economic growth rates are expected to contribute to gradually higher interest rates in coming quarters.

- Holders of shorter-term bond maturities have better opportunities when go-forward rates rise on new bond issuances. Near-term price headwinds will be muted as a transitory rise in rates accompany gradual economic recovery from the pandemic.

- Rising rates will likely benefit floating rate bank loans and high yield bonds because their coupons are higher than investment grade bonds and price valuations would benefit from improving economic conditions. Generally, credit markets appear healthy with tight spreads and limited defaults.

- Emerging Market Debt (EMD) have lower relative prices when compared to developed markets as low vaccine access, reduced growth expectations, and indications of accommodating Central Bank policies are likely to lessen short-term negative volatility.

- The European Central Bank (ECB) indicated that slowing growth and higher inflation could delay any significant discussion about higher interest rates for the next couple of years.

Equity

- The S&P 500 equity index marched higher in October and into November amid strong third quarter earnings reports. (See Market Tracker below.)

- An equity risk-premium is an excess return earned by an investor when they invest in the stock market over a risk-free rate (Government bonds and cash). This return compensates investors for taking on the higher risk of equity investing.

- Going forward, equity returns may be lower when compared to the last couple of years because of (post-pandemic) slower earnings growth, elevated valuations, and increasingly restrictive monetary policy. However, a positive equity risk premium and stronger consumer confidence will likely serve to keep equities relatively appealing in the near future.

- In particular, small-cap value companies may benefit from higher rates, reflation, attractive relative valuations, and the normalization of supply chains and labor markets.

- Volatility is expected to be elevated as Chinese real estate defaults and a recalibration to a new regulatory environment will likely create a headwind for emerging markets.

- Investors should remain prudent, flexible, and balanced in equity allocations while being prepared for potential volatility across equity and fixed income allocations.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.