U.S. Economic and Market Highlights

The Economy:

- The Federal Reserve narrative changed to a more hawkish tone regarding short-term interest rates as Chairman Powell said they may need to increase interest rates sooner than originally expected. This is likely to start with the Fed tapering its bond purchasing program.

- Higher GDP growth rates and inflation tendencies also prompted other Central Banks to take more aggressive positions on combating inflation, including Canada, New Zealand, Brazil, Mexico, Norway, and Russia.

- The result of a more hawkish outlook is a stronger U.S. Dollar (and other currencies) compared to the Euro, as the European Central Bank (ECB) continued to take a more dovish outlook on raising interest rates, as the vaccination and reopening process has accelerated less rapidly in Europe than in the U.S..

- The Consumer Price Index (CPI) increased 5 percent in U.S. from May 2020 to May 2021. It was the biggest jump in nearly 13 years, as the economy rebounded from Covid-19. But there are reasons to expect inflation rates to level off after the immediate recovery rebound including a persistent global savings glut; aging populations; and advances in technology which are all expected to temper long-term inflation.

Fixed Income:

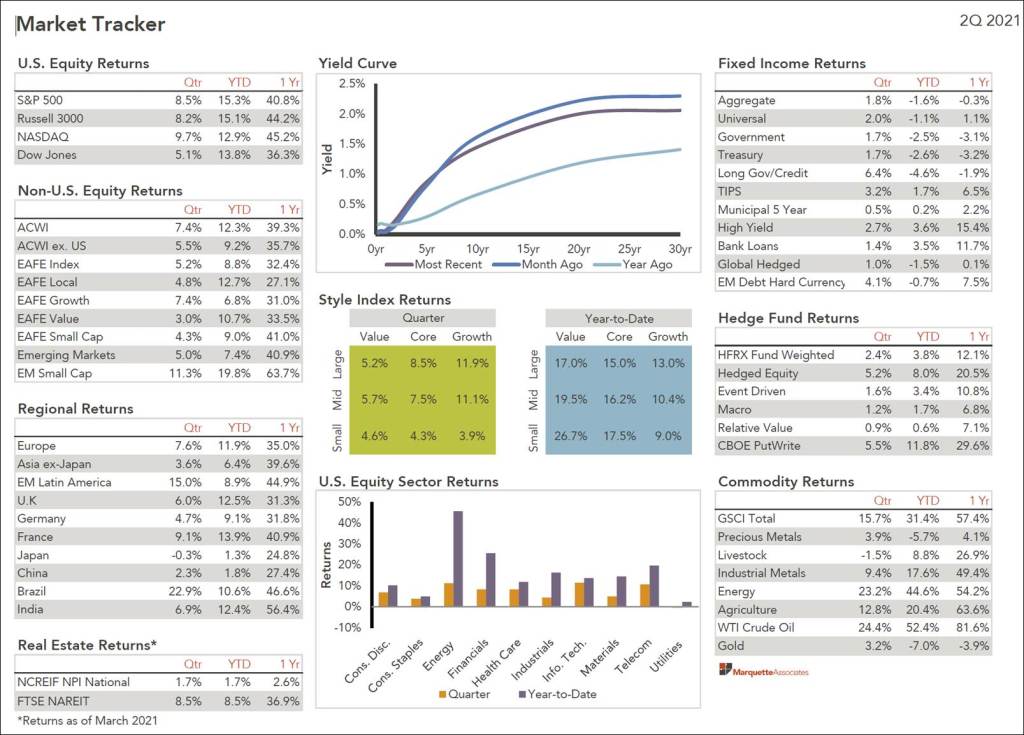

- Long-term yields were lower on the benchmark 10-year Treasury Note even in light of the potential for earlier than expected higher short-term interest rates.

- Reasons for lower long-term yields include an abundance of liquidity in the financial system, in part because banks are purchasing Treasury bonds rather than making loans and recycling money back into government securities.

- Bank savings account balances have increased as a result of the pandemic and influx of government stimulus and recovery allotments.

- These conditions contribute to easier financial conditions and create a favorable backdrop for equities and other risk assets.

- Even with lower long-term rates on U.S. government bonds, U.S. rates are higher than those in other developed markets and therefore demand for U.S. Treasuries is likely to continue.

- The premium between corporate debt and U.S. Treasuries has dropped to its lowest level in more than a decade in a sign that investors are growing confident that recent rises in inflation will not hinder the economic recovery.

Equities:

- In June, the S&P 500 rose for a fifth straight month, notching its latest all-time high to close out June, while equity market volatility has remained steady with the VIX (volatility index) remaining near long-term average levels.

- Large-cap growth stocks outperformed value stocks in the second quarter, while value outperformed growth stocks year-to-date and in the small-cap company universe (see Market Tracker below).

- Investors are prudent to hold both growth and value companies as the economy moves from the early recovery cycle to mid recovery cycle. The financial and consumer discretionary sectors experienced the sharpest rebound in earnings growth and profits year-over-year ending in June.

- China’s equity market has lagged so far this year because of the high weighting toward technology stocks and concerns about slowing credit growth in China. This should start to reverse later in the year as Chinese credit growth stabilizes and vaccines become more available across emerging markets.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.