U.S. Economic and Market Highlights

The Economy:

- The rise in GDP reflected an acceleration of the economic recovery and was sparked by a 10.7% surge in consumer expenditures, which is the largest component of the U.S. domestic economy. Similar trends are evident in Europe, just lagging the U.S. by several months.

- The broad commodity price increase has been driven by an acceleration of global economic growth, improving consumer confidence, rising housing prices, and instances of supply constraints.

- Sales of existing homes were up 12.3% on a year-over-year basis in the U.S.. A combination of low mortgage rates and constrained supply has propelled the median sales price of an existing home to record highs. Average home in America is $329,100 compared to $280,700 one year ago.

- Economic activity in the U.S. accelerated in the first quarter at an annualized GDP pace of 6.4%, slightly slower than the median Bloomberg forecast of 6.7%.

- Unemployment rates fell in most countries with India being an exception as their unemployment rate reached a one year high, up significantly since April due to the recent COVID-19 wave.

Fixed Income:

- U.S. Ten-year Treasury yields rose about 1% from the start of Quantitative Easing (QE) last spring. Equally important is that in previous QE cycles ten-year yields fell toward the end of the cycle, resulting in a flattened yield curve.

- Current ten-year bond yields in Europe are still negative although expected to rise by 30 to 40 basis points by the end of 2021 with accelerating economic activity.

- Fixed income segments added more credit risk in the last 12 months. Indexes representing the U.S. Treasury and Agency markets recorded modest declines. Indexes representing U.S. high yield and emerging markets bonds posted strong returns, navigating somewhat different operating environments.

Equities:

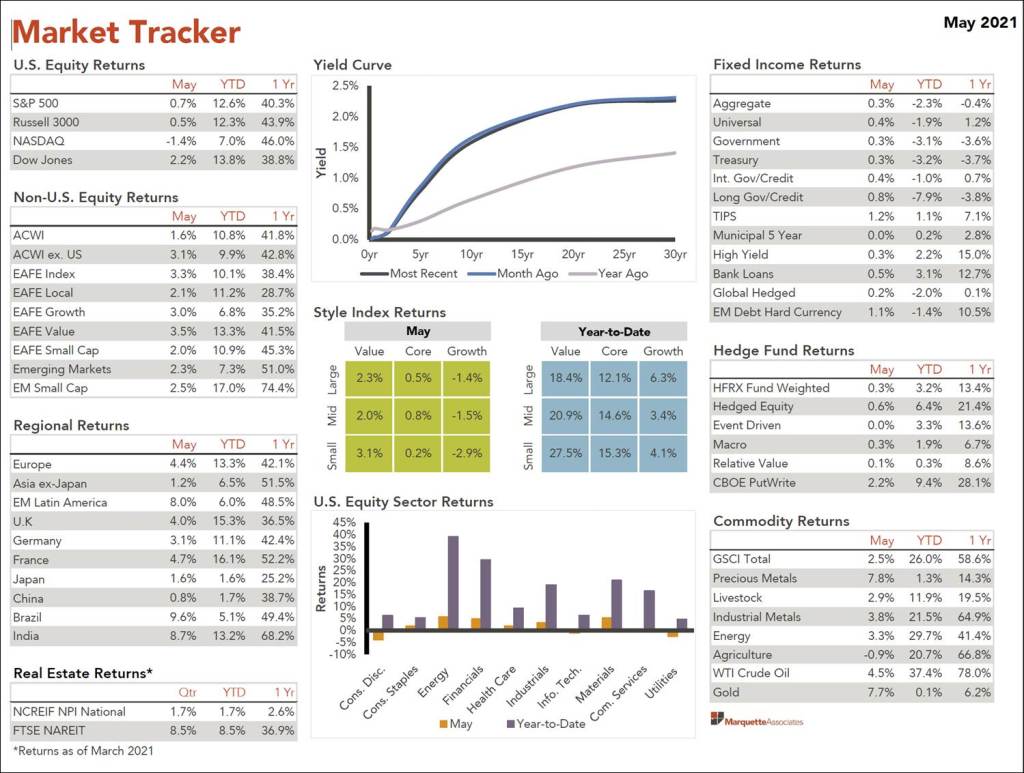

- Equity markets had mixed returns in May with the best performance in Latin America, Brazil, and India following a strong global equity market performance in April. (See Market Tracker chart below.)

- The rotation into cyclical value stocks took a breather in April as growth stocks regained market leadership. In April, the S&P 500 Growth index outperformed the S&P 500 Value index for the first month this year.

- Moderately lower interest rates and impressive earnings reports helped some mega capitalization stocks post double-digit monthly returns.

- Current West Texas Crude Oil (WTI) is approximately 78% higher than a year ago at $69.62 per barrel; Gold is 6.2% higher at $1,894 per ounce, and Bitcoin is up more than 2.5 times its price one year ago at $35,867.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.