U.S. Economic and Market Highlights

THE ECONOMY:

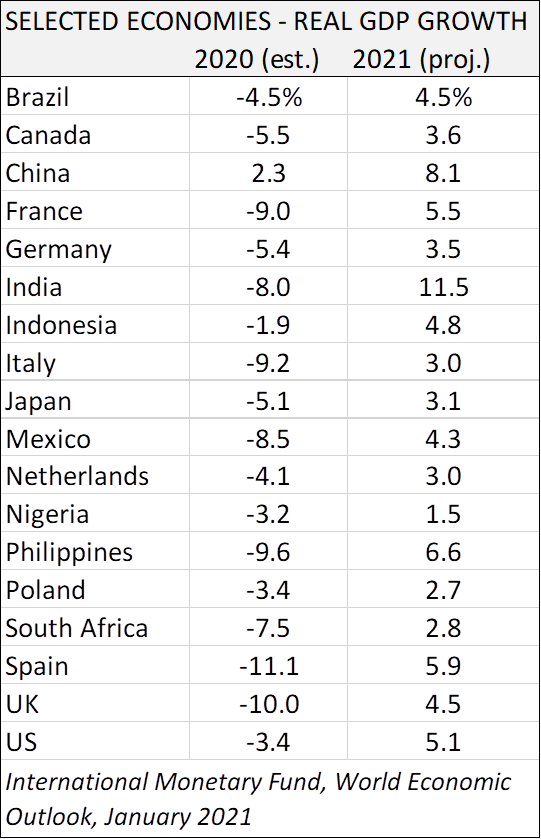

- Recent vaccine approvals raised hopes for a turnaround in the pandemic later this year. Although renewed waves of the virus pose concerns for the outlook. Amid this uncertainty, the global economy is projected to grow 5.5 percent in 2021, reflecting expectations for strengthening economic activity and additional policy support in a few large economies.

- This projection follows a severe global contraction in 2020 of -3.5% which had acute adverse impacts on women, youth, the poor, the informally employed, and those who work in contact-intensive sectors.

- The strength of the recovery is projected to vary significantly across countries, depending on access to medical interventions, effectiveness of policy support, exposure to cross-country population spillovers, and economic structural characteristics.

FIXED INCOME:

- Additional fiscal stimulus from the U.S. Congress and E.U. Parliament spurred an increase in long-term interest rates in January,which negatively impacted government bond prices.

- On the other hand, investment-grade corporate bonds are trading at relatively high prices (i.e., tighter spreads) due to increased issuances and purchasing volumes.

- Investors who are willing to take on more risks are considering high yield bonds, private credit, and real estate assets with lower prices to try to earn higher returns over time.

- The decreasing U.S. Dollar exchange rate has made non-USD denominated bonds more attractive.

EQUITIES:

- The stock market ended 2020 with the best quarterly market performance since 2009. The new year started much the same way except for the last week of January when stock prices fell causing a small negative return for the month of January.

- Emerging markets were the exception in January with positive returns due to overweight positions in Asian companies which make up 75% of the MSCI Emerging Market Index (China 39%, South Korea 13.5%, Taiwan 12.8%, and India 9.3%).

- The stock market rally for most of 2020 was driven by technology and communication services, growth stocks. However, value companies have made a recent comeback outperforming growth companiesin the fourth quarter and in January, which helped strengthen the breadth of the market recovery and benefitted a broader investor base. (See Market Tracker below.)

COMMODITIES:

- Over the last two quarters, according to the SDCI index universe, 26 of 27 commodities had positive returns for the first time since 1991.

- The weaker U.S. Dollar helped to prompt increased investor interest in metals as spot gold and silver prices continued to rise.

- Oil and gas prices also rose due to the weaker USD, opening of the economy, rising stock markets, supply constraints, and higher winter heating demands in the north.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.