U.S. Economic and Market Highlights

The Economy:

- Activity in the manufacturing and service sectors rose for the seventh consecutive month since the economy reopened last May after the COVID-19 outbreak.

- However, the U.S. labor market lost 140,000 jobs in December as a resurgence of COVID-19 cases ended seven months of job growth. The unemployment rate held steady at 6.7%, far better than the April peak of 14.8%, but still almost twice the pre-pandemic level.

- The Fed’s modified inflation policy to delay raising rates should be favorable for equities and corporate bonds and lengthen the business cycle.

- The U.S. dollar is currently hovering around lows not seen since April 2018 with EUR/USD exchange at 1.22. Analysts expect USD weakness to persist into 2021.

- The reason for the downside momentum for the dollar is a combination of vaccine progress, Joe Biden’s U.S. election victory, another possible coronavirus aid package, the Fed’s commitment to maintaining low interest rates, and investors move back into riskier assets.

Fixed Income:

- Fixed income values were stable in November and December as long-term rates stayed well below 1% due to the uncertainty caused by recurring COVID-19 concerns, and its potential negative economic impact.

- Investment grade bonds have provided dependable, but low, returns and are trading at high prices. High yield bonds are trading at lower prices with higher rates and higher risk. But they have the potential for better returns especially because high yield default rates have declined significantly since the initial virus outbreak.

- High yield bonds have a higher risk profile than investment grade bonds because of their lower credit ratings. But they have a lower risk profile than stocks.

- The outlook for emerging market bonds is positive going into 2021 because most of the emerging market bond issuances are coming from Asia, and they have had better success managing the virus with less negative economic impact.

- During the first week of the new year the 10-year Treasury Bond rate jumped to 1.13% from 0.91% because of the increased likelihood for more government stimulus under a Democrat administration.

Equity:

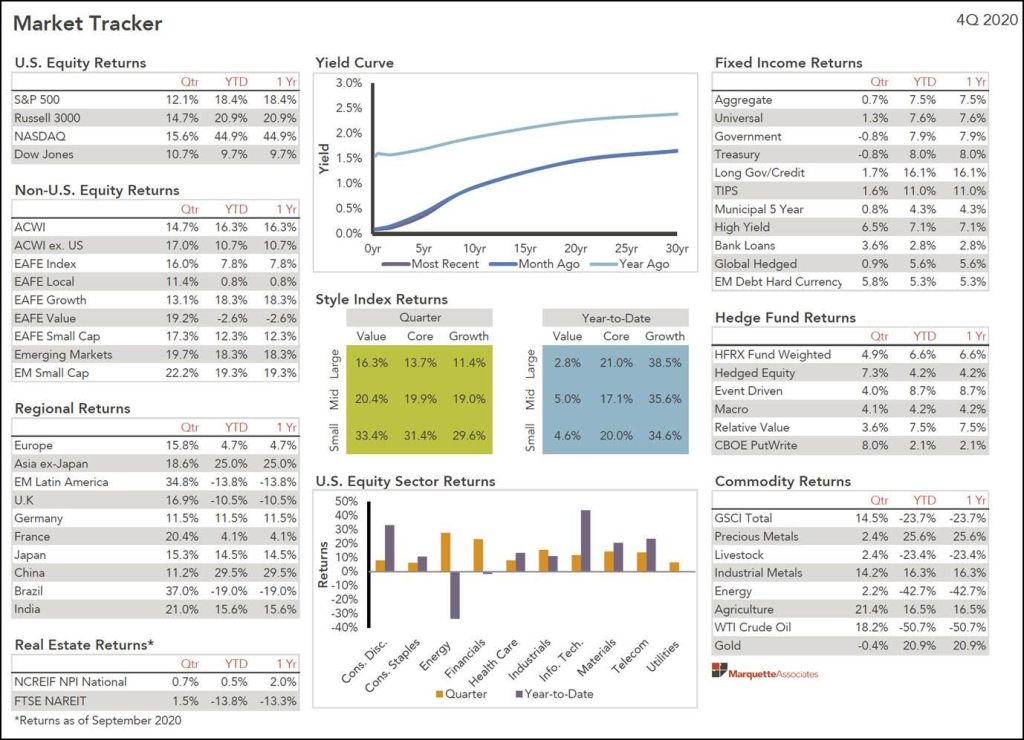

- Stock market returns recovered in 2020 from a five week drop of more than -34%, after the coronavirus outbreak, to a double digit return of 18.4% for the year. See Market Tracker below.

- The Technology sector in the U.S. and Asia outperformed other sectors to lead the rebound, driving up (price/earnings) valuations above average, especially for growth stocks.

- Stock market volatility (VIX) subsided in conjunction with the rebound and dropped back to the long-term average after the U.S. election resolution and continuing vaccine optimism.

- Companies’ earnings for the year were far better than analysts initially estimated after the virus outbreak. Around 85% of companies reported earnings above analysts’ estimates which is the highest in 30 years.

- Small-cap, value, and non-U.S. stocks outperformed in the fourth quarter broadening the scope of the rebound.

- U.S. stocks (represented by the Russell 3000 Index) have outperformed the last ten years. Previously, non-U.S. stocks (represented by ACWI ex U.S. IMI index) outperformed for seven years.

Other:

- Oil prices rose to a 10‐month high after Saudi Arabia surprised the market with a large cut in crude oil production.

- The new U.S. Administration has committed to rejoining the Paris Climate Agreement.

- U.S. China tensions are rising over disagreements regarding the sovereignty of Taiwan.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.