U.S. Economic and Market Highlights

- U.S. Stock market return in January (via the S&P 500) was up almost 8% (best January since 1987) after being down 9% in December (worst December since 1931).

- Since the start of the new year stock markets continued to be volatile but mostly positive on good news about U.S. employment, continuing trade talks with China, and a wait and see approach by the Fed toward raising interest rates.

- The stock market rally in January was welcome following the worst Christmas Eve performance in history and the significant correction in December resulting in negative stock market returns for the year 2018, along with negative returns from other asset classes including non-U.S. fixed income securities.

- Lower inflation, especially gasoline prices, and the prospects for slowing global economic growth brought down interest rate expectations. The 10-year U.S. Treasury Bond rate dropped to near 12-month lows in January which further flattened the yield curve.

- With positive corporate earnings being reported for the fourth quarter, stock market momentum continued positively throughout January, even though consumer confidence forecasts fell significantly as the partial government shut-down sparked fears regarding workers’ claims and long-term negative residual effects.

- A slowdown in the U.S. housing market continued as existing home sales declined 10% on a year-over-year basis, in part because of rising interest rates last year which seem to have met a near-term peak.

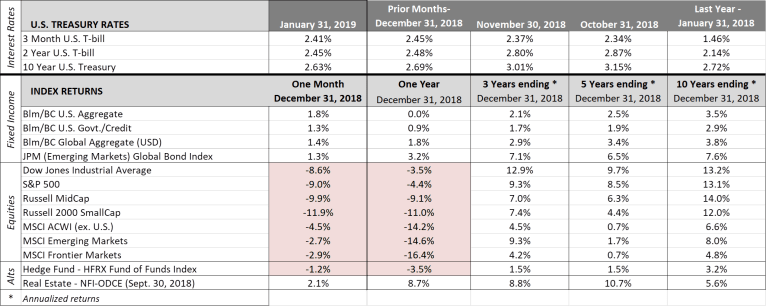

- The correction in equities in the fourth quarter of -13.5%, was significant when measured in the short-term. But higher-risk asset classes, intended for longer-term appreciation such as equities, should also be measured over longer-term periods. See annualized returns in the table below for various asset classes over different periods.

- Investment-grade corporate bonds also lost value in December as the stock market sold-off on concerns about a trade war and slowing global growth. Emerging market debt and equities continued to face challenges as the U.S. dollar maintained strength against other currencies, but with less potential for continued strengthening with the Fed’s decision to slow-down rate increases.

- Treasury, agency, and mortgage-backed bonds that are sensitive to interest rates rallied in December and January as long-term rates declined.

- The overall outlook in the U.S. is for continued growth, albeit at a slower pace in 2019. Most leading indicators are positive and do not suggest a near-term recession. However, we are likely in the late stages of the economic cycle and economic growth around the globe has been slowing, in some cases significantly (i.e. China).

- Additional obstacles that are evident which could accelerate economic decline include: a major trade-war with China, a failed hard-Brexit, a systemic impasse between the White House and U.S. Congress, not to mention the unknown factors that will influence activities and results in 2019.

- That is why we encourage you to review your time-horizon for investing (including the need for income and growth) and determine the appropriate mix of stocks, bonds, and alternatives that match-up with your time horizon. With a longer-term perspective you will better be able to take advantage of down markets by rebalancing in a timely manner, accumulating more investments at lower prices, and being better positioned for future gains.

- See the attached Periodic Table of Investment Returns which shows shifting asset classes over the years, as certain investments move in and out of favor relative to others.

The above was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.