U.S. Economic and Market Highlights

The U.S. Economy:

- Most economic leading indicators continued an upward trend in November, but at a slower pace, following the previous monthly upward revisions.

- Even though rapid growth since the beginning of the year has slowed, economic indicators show a strong likelihood for healthy levels of economic activity in the first half of 2019, while short-term consumer sentiment may suffer due to the federal government shutdown.

- The housing market is one area that is experiencing a negative trend with home sales for November falling below consensus expectations and contracting from the same period a year ago.

- Analysts are forecasting slower growth rates for corporate earnings in 2019, than in 2018.

Fixed Income:

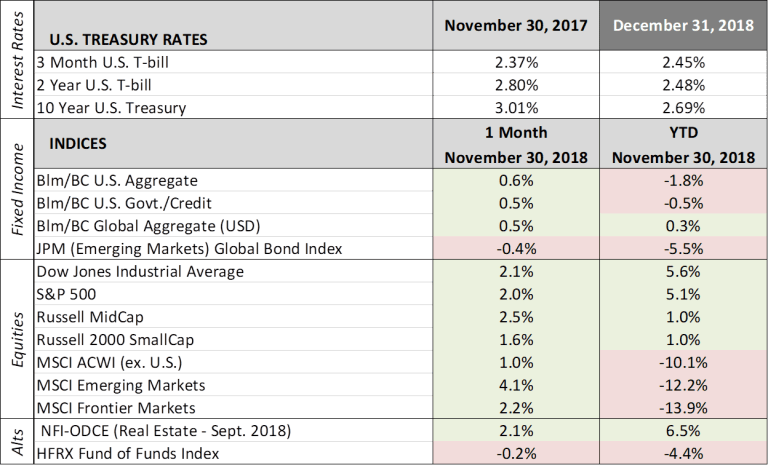

- The Federal Reserve raised its benchmark interest rate in December by a quarter percentage point to 2.50%, but lowered its projections for future rate hikes, while signaling greater flexibility in the central bank’s pace of future interest rate hikes.

- The yield curve flattened as the difference between short-term and long-term rates narrowed. The 10-year Treasury note dropped 32bps, to 2.69% on December 31st, leading to a bond rally in December.

- High yield bonds and U.S. Agency bonds experienced positive YTD returns when most fixed income categories have been negative YTD through November.

- Emerging market bonds were the worst performing fixed income category by a significant margin as the U.S. dollar maintained its strength in November.

Equity Markets:

- December was a volatile month resulting in negative returns across the equity market spectrum due to concerns about: a slow-down in tech stock performance, U.S. government shutdown, a Federal Reserve viewed as too aggressive, continued trade tensions with China, and signs of slowing global growth.

- The S&P 500 (U.S. stock index) ended the year down -6.2% in 2018, and the MSCI ACWI ex. U.S. (World stock index excluding the U.S.) was down -14.2%, which is the worst performing year since the 2008 financial crisis for both indices.

- The table below now shows the MSCI Frontier Market Index which includes investable countries, of the developing world, with equity markets that are smaller and less accessible, or pre-emerging markets for investors that seek to pursue higher, long-run return potential as well as low correlations with other more developed markets.

Alternatives:

- The price of U.S. crude oil has fallen significantly in the past six months from $73.94 per barrel on July 2 to $45.41 on December 31, 2018.

- Bitcoin has declined about 75% from its all-time highs in less than one year (even though it is not certain how Bitcoin should be categorized; as a security, form of payment, or something else).

- For investors who have worked with their advisors and determined the appropriate mix of stocks, bonds, and alternatives that match up with their time horizon, down markets ought not be feared, but rather viewed as an opportunity to rebalance, accumulate more securities at lower cost, and be better positioned for gains when the eventual next bull market occurs.

The above was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.