U.S. Economic and Market Highlights

- The year-over-year reading for Core Personal Consumption Expenditure (PCE) rose to 2.0%. This is the Fed’s preferred inflation measure and is right on target.

- However, given that U.S. GDP growth rising above a 3.5% annualized rate in the third quarter the expectation is for inflation to rise above the Fed’s target rate.

- Rising wages could add upward pressure on inflation, which will give the Fed further support to continue raising interest rates. Average hourly earnings rose 2.8% year-over-year as of September 30.

- Inflationary momentum will be closely watched by the Fed, and investors, as an important indicator of near-term, economic growth trends. In question is whether consumer demands and economic growth will drive prices higher or if growth will stall and indicate an economic slow-down, or recession.

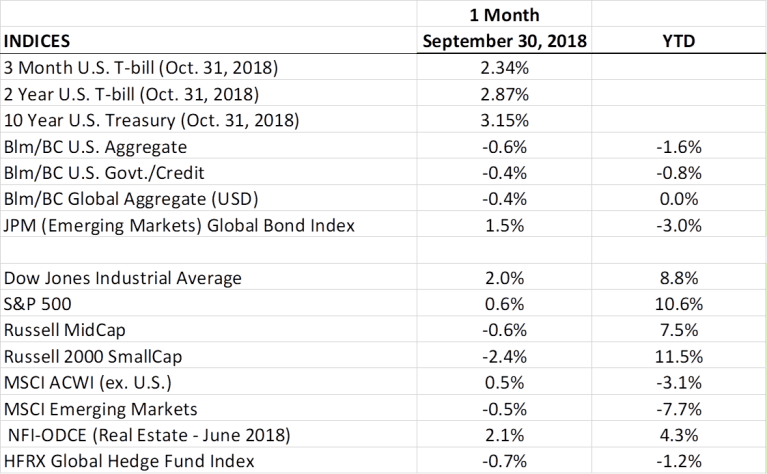

- In September, the U.S. stock market gained to record highs for a second consecutive month. Small-cap U.S. stocks outperformed other indices. While the Emerging Market indices fell in September amid concerns about weakening currencies and high levels of dollar denominated debt in a few countries.

- October was a different story, stock markets declined in the month, bringing index averages to slightly positive year-to-date, while experiencing significantly more than average volatility.

- A primary bearers of the correction was the previously high-flying technology and consumer discretionary sectors.

- The higher growth rates from the previous quarters and the Fed’s indication of higher interest rates to come prompted a significant rise in (longer-term) U.S. Treasury bond yields. Yields on the benchmark 10-year Treasury bond climbed from around 3.0% to 3.23%, marking their highest levels since May 2011.

- As rates rise, market prices on existing bonds are negatively impacted. The result is that U.S. Treasuries, agencies, investment-grade corporates, and emerging market bonds have all had negative 12-month returns. (High yield and municipal bonds were the exceptions with positive 12-month returns.)

- Additional fervor for the stock market sell-off was the forecast for weaker global growth from the IMF, and continued trade tensions between the U.S. and China.

- But third quarter earnings reports are showing renewed focus on strong corporate earnings, especially at the banks.

- The increased volatility in the stock market in October created a temporary rally in safe-haven assets including gold and U.S. Treasury bonds, with rates on the longer-term bonds coming down off the recent highs.

- One weak economic trend that has continued for the last six months is the U.S. housing market whose sales declined again in September, in part due to higher mortgage rates.

The above was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.