U.S. Economic and Market Highlights

- The U.S. GDP grew at a revised 4.2% annualized rate in the second quarter.

- The unemployment rate remained at 3.9%, in the U.S., slightly above its lowest level since 1969.

- Average hourly earnings increased 2.9% year over year, a growth rate not seen since 2009.

- Rising wages could add upward pressure on inflation, which will give the Fed further support to continue raising the Fed Funds rate, which was increased to 2.25% on September 26th.

- Consumer confidence increased in the U.S. to near record highs in September.

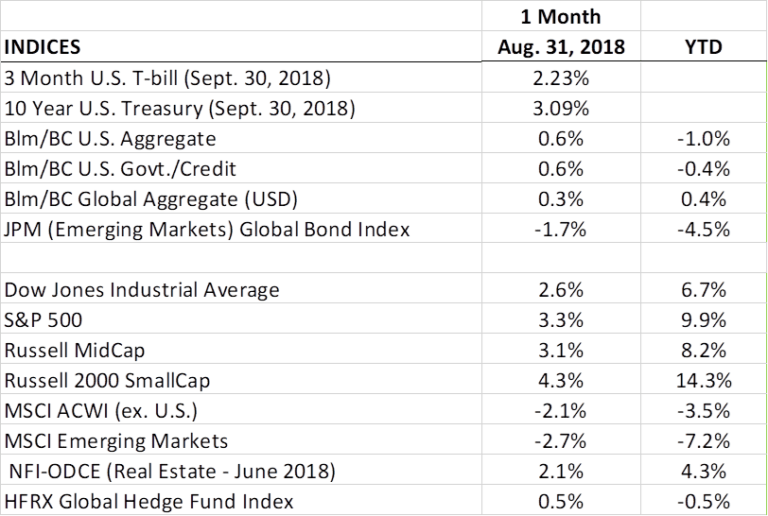

- The resilient U.S. economy propelled domestic stocks to another strong month. The S&P 500 Index and Dow Jones Industrial Average reached all-time highs in mid-September.

- Analysts are forecasting continued strength this year from company earnings growth and slightly slower growth moving into 2019.

- Emerging Market indices fell in August amid concerns about weakening currencies and high levels of dollar denominated debt. And concerns about banking exposure to emerging market countries weighed on stocks in Europe, as the MSCI Europe stock index declined 3.2% and European Bank stocks index fell 8.6%.

- The European Central Bank (ECB) said they plan to begin raising interest rates next fall and end bond purchases this year. The Bank of England (BOE) left interest rates unchanged as expected and highlighted greater uncertainty about the European Union (EU) withdrawal process (Brexit).

- Corporate bond prices increased as corporate spreads on investment grade bonds tightened further.

- The yield on the 10-year U.S. Treasury Bond increased above 3% in September which negatively impacted interest-rate sensitive securities.

- U.S. dollar strength has helped most commodities in 2018. Exceptions are soybean prices which continued their downward trend despite the Trump administration’s July announcement of $12 billion in emergency aid to U.S. farmers that were hurt by European and Chinese tariffs, and gold prices which declined 11.2% from April to August 31.

The above was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.