U.S. Economic and Market Highlights

- Higher inflation was anticipated in the second quarter, but the threat of tariffs and trade wars kept it from accelerating. Core CPI remained steady at 2.2% for the trailing 12 months and headline CPI increased 2.8% with energy prices having risen 11.7% during that time.

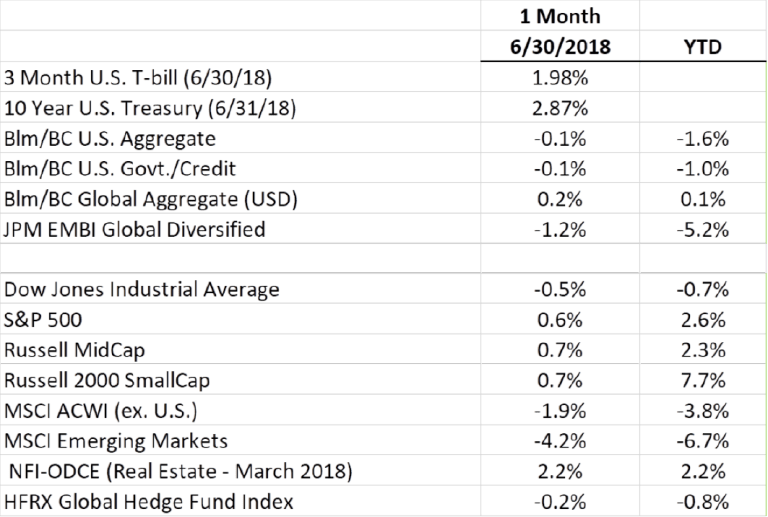

- The trade tariffs created uncertainty and drove investors toward safe-haven investments, primarily fixed income (government and investment grade bonds), which kept the long-term Treasury interest rates from rising.

- However, the Fed increased short-term interest rates in June by 0.25%to the target range of 1.75%-2.00%, resulting in a flattening of the yield curve, which occurs when the yield spread between short-term long term rates and long-term is decreasing. Historically, yield curve inversion has been a reliable indicator of an economic slowdown in the subsequent six to eighteen months.

- It is too early to point to any long-lasting investment implications from the burgeoning trade conflict, several recent developments are notable. First, the Chinese stock market as measured by the Shanghai Composite has declined more than 20% since late January, and the Chinese yuan fell 3.4% in June versus the U.S. dollar.

- The broad U.S. stock market has stayed positive during this period, but the industrial sector struggled in the second quarter as costs of importing parts from China have risen and shares of construction, mining, and aerospace companies have declined.

- So far the S. companies have had a positive year of earnings mainly due to the tax reform and increased government spending. The U.S. economy grew at an annualized GDP rate of 4.1% in the second quarter, marking the fastest economic expansion in nearly four years.

- But tax cuts have not necessarily helped the stock market.S. stocks are incumbered by the uncertainties of the tariffs and trade war and the rising value of the U.S. Dollar against other currencies. While non-U.S. stocks are hindered by slower economic growth in Europe and emerging markets.

- Stock price volatility is up in 2018 more than it has been in recent years, which has created some buying opportunities for active managers.

- Growth stocks, led by technology companies (including the ‘FAANG’ constituents: Facebook, Apple, Amazon, Netflix, and Google) continued to outperform value stocks through 2Q, and only recently saw a correction, which included Facebook being down by 20% in late July, after reporting a decelerating revenue growth outlook.

- Other positive components of the U.S. stock market in the second quarter were small caps companies, private equity funds, and the energy sector.

- International stocks had negative returns in the second quarter, especially those in emerging markets, primarily due to higher short-term interest rates, the strengthening Dollar, continued expectations for stronger economic growth in the U.S.; and uncertainties around Brexit and Italian political changes.

- One, not so bright statistic, is that home sales in the U.S. have declined five out the first six monthsin 2018, which could be a worrying trend, since housing is considered to be a crucial indicator of overall economic health.

The above was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results. Analysis done in cooperation with Cedar Hill Advisors.