U.S. Economic and Market Highlights

The Economy

- Annual inflation in the U.S. ticked higher in March and underlying price pressures remained stubbornly strong (CPI +3.5%), raising further questions about how much the Federal Reserve will be able to cut interest rates this year.

- At the end of 2023, investors expected monetary easing as soon as the spring, with a total of five to six rate cuts for the full calendar year of 2024. That forecast now sits at less than three, and investors currently anticipate a less than 50% chance of a rate cut in the U.S. in June.

- On the positive side, the U.S. labor market continues to surprise economists with its strength, adding more than 300,000 jobs in March alone. Education and health services were the areas of the private market (i.e., non-government jobs) that saw the biggest gains.

- Average hourly earnings in March were up over 4.0% on an annual basis. Forecasts for domestic economic growth remain robust, with economists now expecting U.S. real GDP to increase by more than 2% in 2024.

- Inflation in the 20-nation Euro-zone eased to 2.4% in March, boosting expectations for interest rate cuts to begin in the summer. Most of the major economies were under the Euro-zone average, with the Italian Harmonized Index of Consumer Prices (HICP) at 1.3% on an annual basis, the lowest in the Euro-zone.

- Why is inflation lower in Italy than the rest of Europe? Recent interest rate hikes by the European Central Bank (ECB) dissuaded both firms and households from taking on loans, thereby cooling the economy and effectively tempering inflation. Aggregate loans to Italian households and businesses decreased further in recent months, down -2.6% and -2.7% in January and February 2024, respectively.

- Does this mean a soft landing for Italy’s economy? It depends on the effects of potential interest rate cuts by the ECB this year, which will hopefully stimulate a rebound in economic activity. Italy’s annual GDP is projected to grow by 0.7% in 2024 and is expected to accelerate in 2025 to 1.7% along with business investments.

- The ECB is expected to cut rates in June. This would underscore a decoupling of eurozone inflation dynamics from those in the U.S. With the potential divergence between the U.S. and Europe’s inflation, economic growth, and interest rates, currency strength has tilted toward the U.S. Dollar. The USD compared to other major currencies is up more than 4.6% this year and stands near its highest levels since early November.

Fixed Income

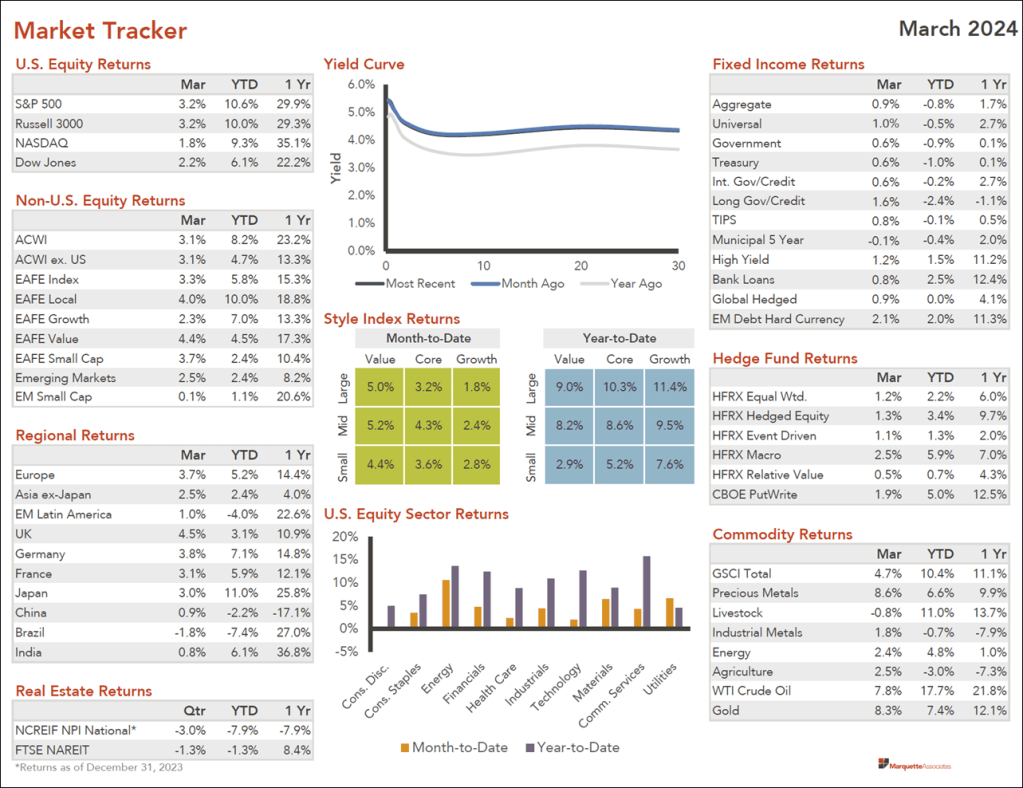

- Higher interest rates in the first quarter pushed rate-sensitive areas of the fixed income market negative. The Bloomberg U.S. Aggregate Bond Index returned -0.8% during the first quarter. (See Market Tracker below.)

- Corporate bond sectors remained resilient as high yield, leveraged loan, and emerging market credit securities were all positive in the first quarter.

- Fixed income remains an attractive asset class, with high starting yields providing compelling income and serving to generate a positive expected total return over the next 12 months under the majority of spread and interest rate scenarios.

- While yields remain attractive, credit spreads are near historical averages and could come under pressure in a recessionary environment. Finally, slower-than-expected rate cuts by the Federal Reserve could be detrimental to bond returns.

- The 10-year U.S. Treasury yield rose 0.40% (40bps) since mid-March and is currently above 4.60% in mid-April. Higher yields generally have a negative impact on the market values of current bond holdings in portfolios.

- Yield spreads have widened on longer-dated bonds between the U.S. 10-year Treasury and the 10-Year German Bund, which currently yields 2.44%, resulting in over a 200 bp spread. The main reason for the higher-than-average spread is the higher-than-expected U.S. inflation rate, which results in a cheaper relative price for the higher yielding U.S. Treasury Bond compared to the same duration German Bund.

- U.S. 30-year mortgage rates rose above 7%, while at the same time refinancing applications rose 10% as homeowners rushed to lock in rates amid concerns that rates could go even higher. The result to investors was a decline in the market prices for agency mortgage-backed securities (MBS) which recently underperformed Treasury fixed income securities.

- When rates decline, high-quality fixed-income bonds of intermediate duration have the potential to generate total returns that are substantially greater than current yields.

Equities

- All major equity indices ended the first quarter in positive territory (except Brazil and China). The S&P 500 achieved multiple all-time highs in the first three months of the year. All major sectors of the index (excluding real estate) were positive in the first quarter.

- There were indications that investors are beginning to expand their focus across the market, as sector leadership was diversified and both growth-oriented sectors like Communication Services and Information Technology led alongside value-oriented sectors like Energy and Financials.

- The Russell 2000, small-cap equity index continued to underperform its larger rivals, while remaining positive. The positive result of their underperformance is that their forward price-to-earnings multiples are relatively low (i.e., prices are cheaper) relative to large-cap indices whose prices remain above historical averages.

- Stock market returns in April in the U.S. have been negative thus far because of higher-than-expected inflation rates. The Fed is not expected to lower interest rates as early as the market had hoped and “higher for longer” rates, lead to increased pricing pressures and chances for a hard-economic landing at the time inflation rates eventually decline.

- The strength of the U.S. Dollar was a headwind for investors in international markets due to the Fed’s maintaining interest rates at elevated levels. Hedge funds had positive returns in the first quarter, as global macro strategies led the way, with the HFRI Macro Index return of 6.9%, which marks the strongest quarterly performance for the index in over 20 years. These strategies benefited from higher commodity prices, as oil, gold, copper, and cocoa prices have all pushed higher.

- Real estate performance declined in the fourth quarter, as investor demand and transaction activity fell in response to the shortage of available financing, continued pressure from elevated interest rates, inflationary pressures, and a bleaker outlook for economic growth.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results. See below reference sources used in preparing the above information.