U.S. Economic and Market Highlights

The Economy:

- Many national governments in Europe and around the world reinstated various lockdown measures, to thwart the second wave of the Coronavirus. The new restrictive measures announced could negatively impact economic growth and outlook for the next several quarters.

- Consumer confidence rose in the U.S. as the U.S. labor market added more jobs than expected and the unemployment rate fell from 7.9% to 6.9% in October.

- The market views the election and split government as a positive. There will be less fiscal stimulus due to the split government, resulting in less of an inflation threat.

- The Federal Reserve recently announced a new policy on its approach to inflation measures by committing to refrain from monetary tightening (i.e. raising interest rates) until inflation stays consistently above its 2% target following periods in which inflation runs below the 2% target.

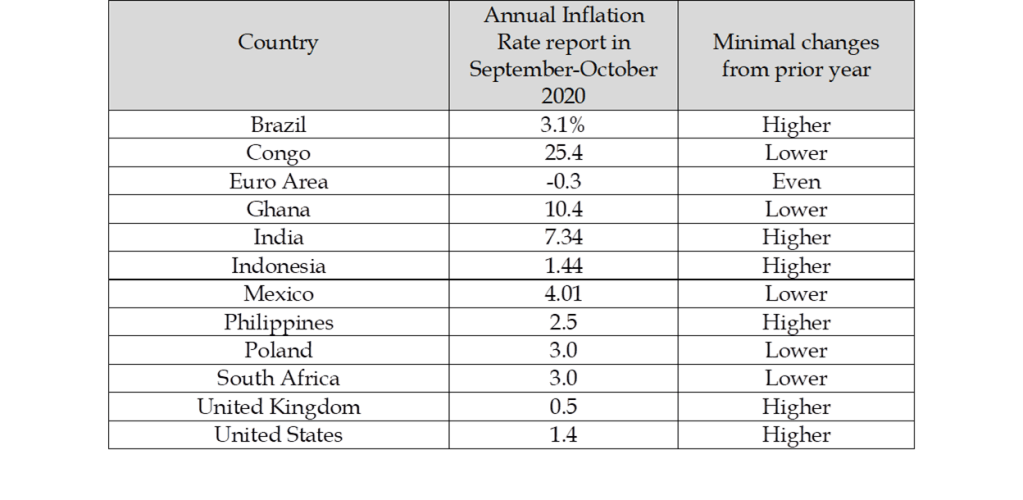

- Below are samples of current inflation rates from around the world.

- Gross Domestic Product (GDP) rebounded at record levels in countries around the globe following a historic contraction in the second quarter. There were exceptions, for example, lockdowns in Indonesia slowed its economy in the third quarter to recessionary levels resulting in a negative GDP rate of -3.5%.

- Forecasted GDP growth rates in 2021 are 5.2% globally and 3.7% in the U.S.. The difference is partially explained by the respective levels of recovery thus far in 2020.

Fixed Income:

- Corporate bond values continue to increase as demand outpaces supply. Since the Federal Reserve started buying U.S. corporate bonds as part of the stimulus package, bond values have steadily increased (and interest rate spreads have tightened between corporate and government bonds).

- Corporate credit downgrades declined over the last few months and have remained at pre-pandemic levels.

- The government bond yield curve is still near historic lows, as short-term rates remain close to zero in the U.S. and negative in many countries in Europe and in Japan, and slightly higher on longer dated bonds.

Equities:

- The U.S. stock market has outperformed the rest of the world since the initial pandemic outbreak in early 2020 and for most of the last decade. (See Market Tracker below.)

- Currently, the S&P 500 – U.S. Stock Market Index is overvalued when comparing the current Price/Earnings (P/E) ratio of 31.2% versus the historical average of around 16%.

- Recent outperformance has been concentrated for the most part in a handful of big tech giants which have led overall market values beyond what would have otherwise been the case.

- U.S. stocks recorded their largest weekly gain since April as risk assets responded favorably to election results which appear to be heading in the direction of maintaining a split Congress and a Biden presidency. However, the election outcome is still uncertain with vote counts still underway in several key states.

- The prospect of Republicans retaining control of the Senate, and Democrats having a narrower majority in the House of Representatives, would diminish the Democrats’ ability to enact Biden’s proposed agenda, including changes to the corporate tax rate, health care industry, and minimum wage.

Real Assets and Gold :

- If liquidity is important for your funds, then buying gold is not the best investment because the current price and volatility is high, meaning that it has a higher than average probability of going down in value short-term. However, gold and other real assets may have a place in a long-term investment portfolio (to a limited degree <5%) if you are able to buy it at a relatively low price.

- If the virus persists and there is no effective vaccines and government funding programs fail to generate economic growth, gold could rise long-term from here, without dropping much. Alternatively, if there are vaccines and the economy begins to grow again at normal levels, in the not too distant future, gold may drop a while before it reaches new highs.

- There may be a better opportunity to invest in gold when prices are lower, after the “Covid-storm” is over. Perhaps, at that time the markets will realize how much debt governments have taken on and how big the deficits are going to be in years to come. That realization could trigger inflation, which would likely be a good time to own gold, and other real asset, commodities.

This communication was prepared for informational purposes only and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security/instrument or to participate in any trading strategy. Past performance is not indicative of future results.